Indices

Are We Ignoring the Recession Right in Front of Us?

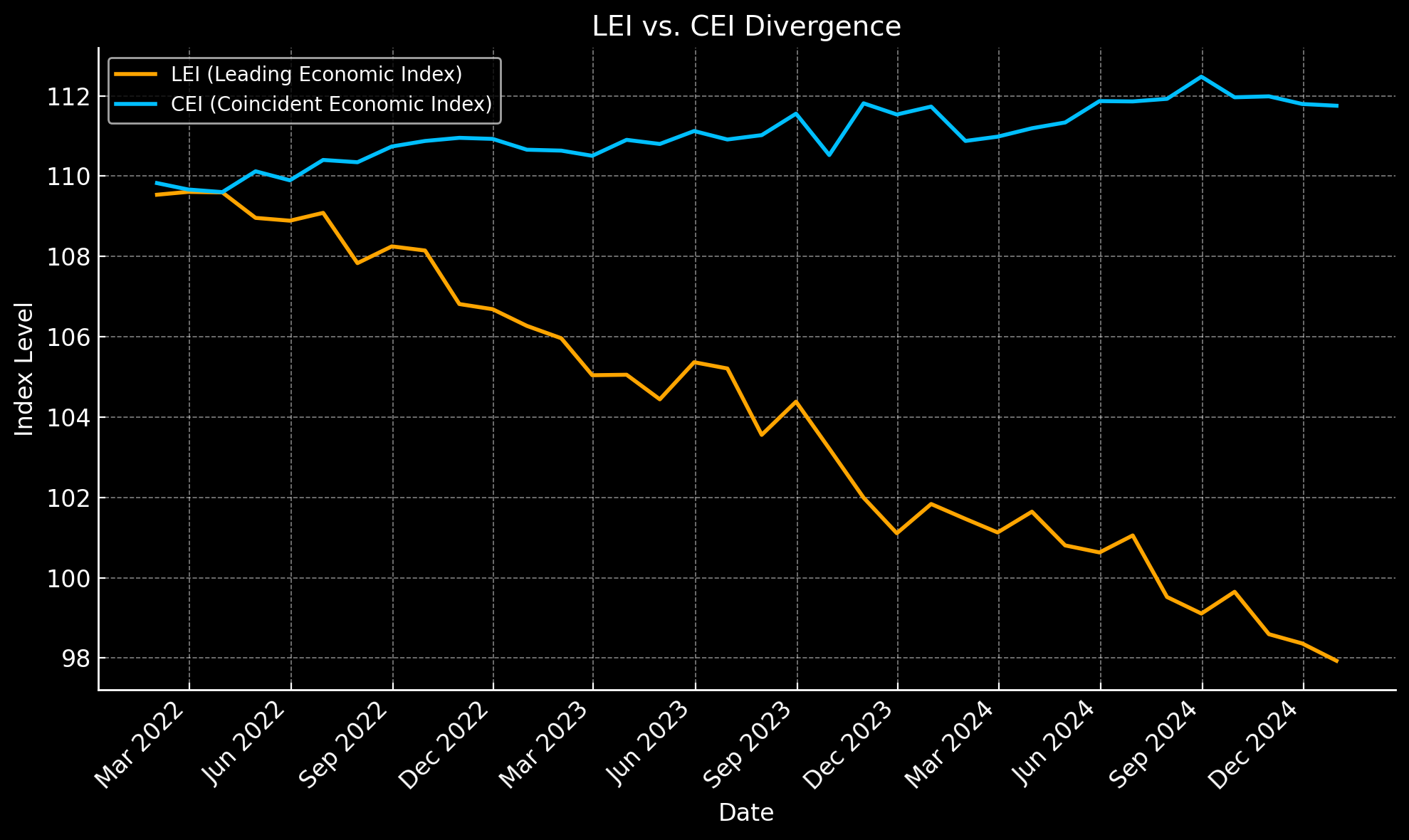

The growing divergence between the LEI and CEI is flashing a classic recession warning, even as current data remains firm. If the CEI starts to turn lower, markets could quickly reprice for a slowdown. Equities remain vulnerable, especially given stretched valuations and limited risk pricing. Investors should monitor CEI closely over the coming months for confirmation. A validated downturn could mark a major turning point for sentiment, positioning, and policy.

The LEI–CEI Divergence: A Warning Signal Markets Shouldn’t Ignore

Over the past year, the U.S. economy has shown remarkable resilience despite persistent macroeconomic uncertainty. Yet beneath the surface, a concerning divergence has emerged between two critical indicators: the Conference Board’s Leading Economic Index (LEI) and the Coincident Economic Index (CEI). While this disconnect has not yet triggered widespread alarm in the financial markets, historical patterns suggest it could be an early warning sign of a potential economic downturn—and one that investors would be wise to monitor closely.

The Divergence: What It Signals

The LEI is designed to forecast future economic activity. It includes forward-looking components such as manufacturing orders, consumer expectations, jobless claims, and building permits. In contrast, the CEI measures the current state of the economy through indicators like nonfarm payrolls, personal income, and industrial production.

In June 2025, the LEI fell by 0.3% to 98.8, marking its third consecutive “recession signal” and continuing a year-long slide. It’s down 2.8% over the first half of the year, reflecting persistent weakness in several leading components. Meanwhile, the CEI rose by 0.3% to 115.1 in June, supported by solid gains in employment, income, and production. This divergence has created a spread between the two indices that may suggest trouble ahead.

It’s worth noting that while the LEI has been falling for some time, the economy has not yet shown broad signs of contraction. However, that’s precisely why this divergence matters. Historically, it’s not until the CEI starts to turn lower—validating the LEI’s message—that a downturn becomes imminent. If the CEI were to decline for a sustained period, it would confirm the LEI’s long-running warning and dramatically shift the market’s expectations.

What This Means for Financial Markets

For now, the financial markets are largely shrugging off the LEI’s persistent weakness. Stock indices remain elevated, reflecting expectations of a soft landing or continued moderate growth. However, this optimism may be misplaced if the CEI—representing real-time economic activity—begins to soften.

Should the CEI turn lower and confirm the LEI’s recession signal, the market’s reaction could be swift and significant. Equities are particularly vulnerable, as perceived weakness would likely trigger a significant correction in the S&P 500, as has occurred in past cycles. Credit spreads would likely widen, reflecting rising default risk and a deteriorating outlook for corporate earnings.

Bond markets, meanwhile, may experience a rally as investors rotate into safe-haven assets. Treasury yields would likely fall in anticipation of Federal Reserve rate cuts. In addition, a confirmed downturn would bolster demand for defensive sectors and high-quality assets, including gold and utilities.

Importantly, sentiment would shift sharply. Currently, investors are largely complacent about recession risk. A turn in the CEI would likely trigger a reassessment of macro risk, leading to increased volatility across asset classes.

Implications for Investors and Policymakers

Financial markets are currently priced for continued economic strength. Equities are at elevated levels, and investor sentiment leans toward a soft landing or no landing at all. A clear confirmation of economic deterioration via a CEI decline could trigger a swift re-pricing in risk assets. Bond markets might rally in anticipation of a policy shift from the Federal Reserve, while credit spreads would likely widen on growing default risk.

For policymakers, the data complicates the outlook. While inflation remains manageable and job growth stable, the LEI’s persistent decline suggests caution is warranted. A turn in the CEI would likely reinforce calls for rate cuts and more accommodative policy.

In conclusion, the divergence between the LEI and CEI should not be ignored. The LEI is already issuing a clear warning, but the CEI has not yet confirmed it. If that confirmation comes, history suggests the market reaction could be swift and severe. For now, this remains a gap between expectation and reality—but one that may soon close.

References

- wsj.com

- www.conference-board.org

Senior Market Specialist

Russell Shor

Russell Shor is a Senior Market Strategist at Tradu, having been promoted to the role in 2025 in recognition of his depth of insight and consistent delivery of high-impact market analysis. He originally joined FXCM in October 2017 as a Senior Market Specialist.

Russell holds an Honours Degree in Economics from the University of South Africa, is a certified FMVA®, and a full member of the Society of Technical Analysts (UK). With over 20 years of experience in financial markets, his work is renowned for its clarity, precision, and strategic value across asset classes.