Shares

Wall Street in turmoil as Trump tariffs take effect: What has happened so far and what to watch next

Trump tariffs and countermeasures by major trading partners like China spark recession fears and Wall Street turmoil, with household names like Apple taking a hit

Sweeping tariffs kick in

The US President announced a slew of reciprocal tariffs on April 2, which he has dubbed as Liberation Day, aiming to raise revenues and bring back manufacturing. These measures included a baseline 10% tariff, alongside a set of country-specific duties, which took effect on Wednesday.

The United Kingdom was subject to the softer 10% baseline, while other major partners were hit harder. The European Union - whose exports to the US totalled $605.76 billion last year - faced a 20% duty. Asian countries also endured steep tariffs, with Japan facing 24% and Vietnam a striking 46%. In response to Chinese countermeasures, President Trump escalated matters further, imposing a 104% tariff on Chinese imports, as confirmed by White House Press Secretary Karoline Levitt. China responded in kind, raising its own tariffs to 84%, intensifying the tit-for-tat between the world's two largest economies.

Some sectors were exempt - pharmaceuticals, semiconductors, energy products, and copper among them - but the President warned more tariffs were coming. Speaking aboard Air Force One a day later, he noted that levies on semiconductors were “starting very soon”, and that duties on pharmaceuticals would be announced “some time in the near future”, while copper was already under investigation. Additionally, the US had already imposed 25% tariffs on imports of steel, aluminium, and 25% levies on passenger vehicles, light trucks, and key automotive parts.

The magnitude of these actions along with countermeasures from various countries like China, undermine global trade and threaten an economic slowdown. Kristalina Georgieva, Director of the International Monetary Fund, warned that these tariffs pose “a significant risk to the global outlook at a time of sluggish growth”.

Domestic implications

Domestically, the impact could be just as damaging, hitting economic activity, employment, and exacerbating already persistent inflationary pressures. The risk of stagflation or even a full-blown recession is rising.

Federal Reserve Chair Jerome Powell acknowledged the possibility of “higher inflation and slower growth”, though he highlighted uncertainty around the “size and duration” of such developments. Former New York Fed Governor Bill Dudley opined Bloomberg that stagflation was the “optimistic scenario”, while former Treasury Secretary Larry Summers warned of recession and job losses. Some business leaders also shared these concerns, with JP Morgan CEO Jamie Dimon referencing “inflationary outcomes” and a “slowdown” in his letter to shareholders.

While hard data still point to a strong economy and resilient labour market, soft data are painting a gloomier picture. US consumer confidence fell to its lowest level since 2021 in March, according to the Conference Board, while the University of Michigan survey showed long-term inflation expectations had surged to their highest since 1993. Business sentiment has also deteriorated, with the S&P 500 PMI indicating weaker outlooks.

Market impact

Escalating tariffs and mounting recession fears reverberate across global markets, with investors turning to safe havens like the Japanese yen, the Swiss franc, and gold. Equity markets in Asia and Europe - including the Nikkei 225 and DAX 40 - are down for the month, oil prices are declining, and emerging-market currencies such as the Chinese yuan and Indian rupee have weakened.

US markets are also feeling the pressure. Despite expectations that inflation and risk aversion might support the currency, the USDollar has actually declined this year, weighed down by recession fears and increased expectations of rate cuts.

Wall Street suffered a sharp sell-off following the 2 April announcements, compounding this year’s losses and signalling a clear reversal from the post-election rally. The S&P 500 has fallen around 15% year-to-date, teetering on the edge of a bear market and further weakness remains likely.

Source: www.tradingview.com

Even though much of the President’s trade plans are now laid out, the picture is not complete. Prospects of more levies, countermeasures by trading partners, potential for tailored deals, and the sheer size of the tariffs can sustain uncertainty and fear, with the VIX having moved higher.

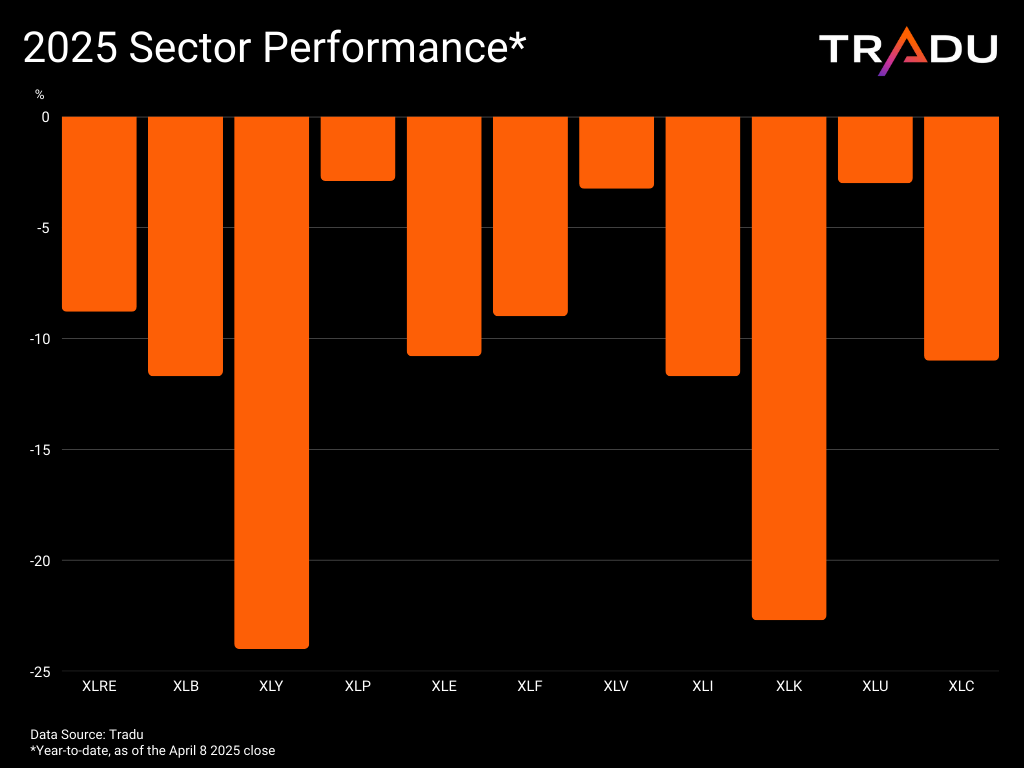

The Consumer Discretionary sector is among the obvious losers, since discretionary purchases are the first to be axed. XLY is among the worst performers of 2025, with its decline exceeding 20%. Within the sector, sportwear makers like Nike are particularly vulnerable Sportswear makers like Nike are particularly exposed, with key production hubs such as Vietnam facing steep tariffs.

Apple faces similar problems due to Asian tariffs and most importantly China. Shares drop approximately 30% this year as the current trade environment can lead to lower margins, higher prices and educed demand. Apple exemplifies the headwinds for Big Tech, with XLK dropping over 20% year-to-date. Tariffs and restrictions on chips exports, as well as China’s curbs on crucial mineral exports come at a time when their AI dominance is challenged by the accelerated efforts of Chinese rivals.

The troubles extend beyond tech. Despite exemptions under the USMCA, US carmakers remain vulnerable due to their global manufacturing footprints and exposure to steel and aluminium duties. Tesla shares have plunged about 45% in 2025, even though the EV giant can emerge as a relative beneficiary of tariffs. Banks are unlikely to go unscathed from the deteriorating macroeconomic environment either, as it could hurt their balance sheets, increase delinquencies, and reduce loan demand.

That said, some sectors are better positioned. Defence companies- bolstered by geopolitical tensions, Trump’s proposed $1 trillion military budget, and "Golden Dome" ambitions - could thrive. Firms like Lockheed Martin, RTX, and Northrop Grumman may benefit. Consumer staples are traditionally resilient in downturns and classic defensive plays, with XPL posting small losses.

What to watch next

Amid mounting macroeconomic pressures and falling stock markets, investors are looking for either a "Trump Put" or a "Fed Put" to stabilise the situation. For now, President Trump appears committed to his tariff strategy, saying that “sometimes you have to take medicine to fix something”.

Meanwhile, Fed Chair Powell reiterated the central bank’s cautious stance to monetary easing, as higher levies can strengthen already elevated price pressures, just as inflation expectations are on the rise. He underscored the obligation to keep such expectations “well anchored” and prevent an ongoing inflation problem.

However, there are signs the administration may be open to compromise. Treasury Secretary Bessent told CNBC on Tuesday that the White House was prioritising certain countries for negotiation and hinted at “good deals” in the pipeline. President Trump has also indicated a willingness to make deals if important concessions are offered, emphasising the negotiating power that tariffs provide.

Although uncertainty is set to persist, discussions with trading partners and openness to deals can go a long way in improving sentiment. Progress on this issue can also allow the administration to turn its attention to other parts of its agenda which are more market-friendly like deregulation and tax cuts. Furthermore, if the economy takes a hit and consumers begin to pull back, the Fed could resume its rate cutting cycle to offer relief, with ample room for easing.

Despite the prevailing gloom and ongoing market weakness, recovery remains possible. The intensity of the sell-off is concerning, but steep corrections are not uncommon following extended rallies. Lower valuations may rekindle interest in blue-chip stocks, laying the groundwork for a potential rebound.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.