Shares

What’s Next for Electric Vehicles:Trends and Innovations for 2025

A Challenging Backdrop for EVs:

Navigating 2024's Struggles and 2025's Opportunities

This has been a difficult year for the electric vehicle industry due to unfavorable macroeconomic conditions. Consumers in many parts of the world grappled with elevated inflation, which reduced disposable incomes, and economic uncertainty, which deterred big-ticket purchases like cars. High interest rates also made the already expensive EVs even harder to afford. Additionally, range anxiety and low resale values continue to weigh on potential buyers. A broader "greenlash" has also emerged, where financially strained consumers are less inclined to bear the cost of the clean energy transition. This sentiment was reflected in the EU Parliament elections [1], where the Greens/EFA alliance lost 17 seats.

This unfavorable set of factors has diminished the appeal of battery electric vehicles (BEV) and has renewed interest for hybrids. Registration of pure BEVs in the European Union dropped [2] 5.8% y/y in the first nine months of the year, just as hybrids rose 20.1% (full and mild) according to the European Automobile Manufacturers' Association (ACEA). This shift makes automakers operating in the continent worried about meeting their 2025 emissions goals, which would incur hefty fines. The UK market appears more resilient with a 13.2% rise in BEV sales but that's much slower than last year's growth. Furthermore, manufacturers struggle with their zero-emission vehicle mandate there too. In the US, sales increased 8.7% y/y in the first nine months according [3] to the Kelley Blue Book, but that's a notable deceleration from 2023 and the nearly 50% rise. China remains the industry's bright spot, as New Energy Vehicles (BEV, PHEV, EREV, FCEV) made up over 50% [4] of total sales in October, a milestone first reached over the summer. NEV sales were up [5] 32.5% y/y in the January-September period.

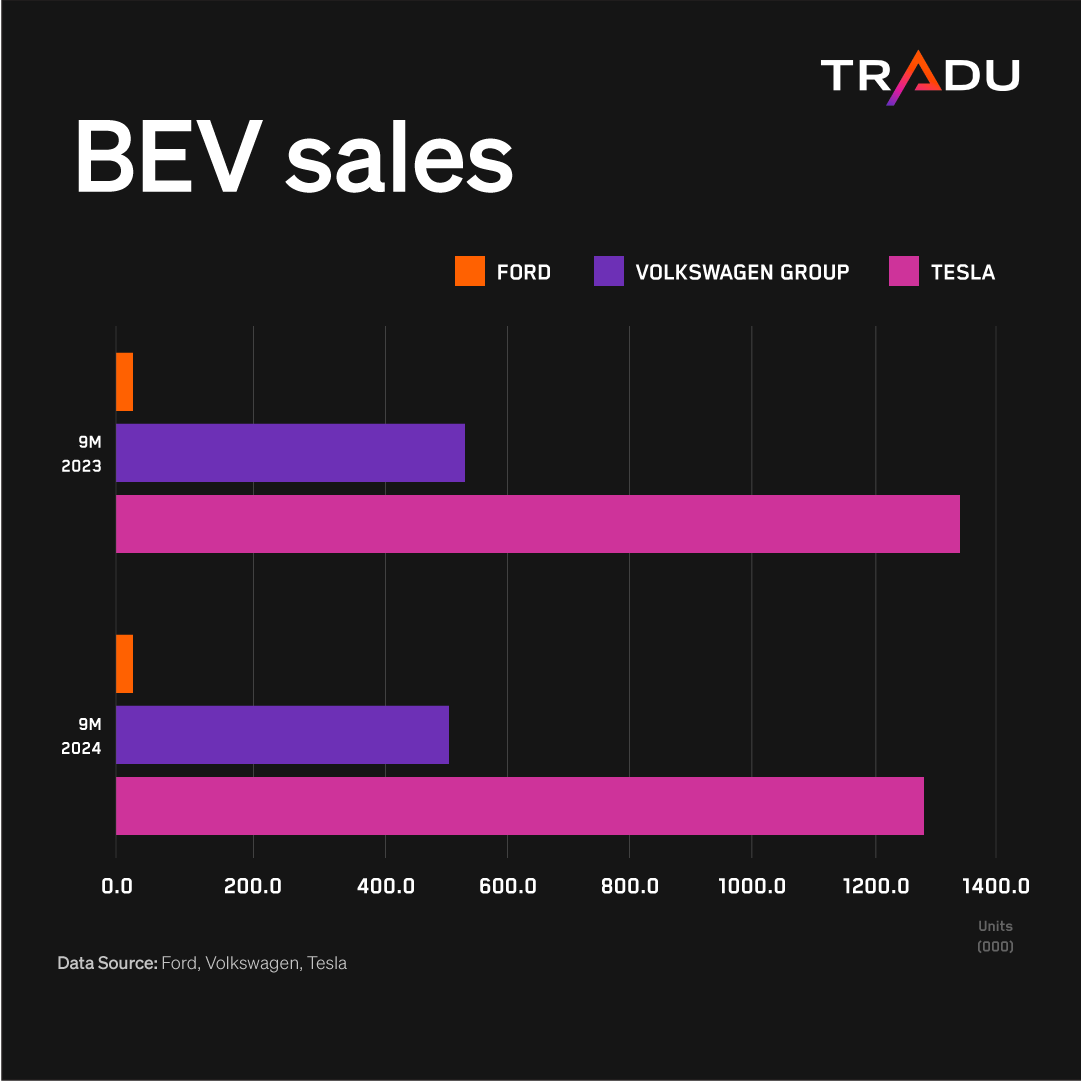

Highlighting this downturn in demand for pure battery electric vehicles, Ford (F.us) sales dropped 17% y/y in the January-September period and German giant Volkswagen Group (VOW.de) reported a 4.7% slide compared to the previous year. EV King Tesla (TSLA.us) experienced an uptick in recent quarters, but still delivered 2% fewer vehicles and is due for just "slight growth" [6] for the whole of 2024.

EV Demand in 2025:

Recovery or Continued Softness?

It is clear that the industry faces a difficult backdrop as the new year gets underway. Existing issues are unlikely to disappear and fresh challenges could be in store, but there are reasons for optimism, making 2025 a transitional year.

The biggest risk emanates from the White House, as its next occupant has a pro-fossil fuels agenda and could slow the shift towards net-zero. President Trump has pledged [7] to unravel the green energy policies of his predecessor and the $7,500 federal tax credit for EVs under the Inflation Reduction Act is in jeopardy, with profound implications for the already struggling market. Recent research [8] titled "The Effects of Buy American: Electric Vehicles and the Inflation Reduction Act", suggests that such repeal would lead to a 27% plunge in EV registrations in the US.

Another hurdle to the proliferation of EVs comes from frail Sino-Western relations and import tariffs in the US and Europe. The European Union has imposed [9] countervailing duties on Chinese BEVs of up to 35.5% (on top of the preexisting 10% levy). The Biden Administration in the US has implemented [10] 100% tariffs, essentially barring the entry of Chinese vehicles. There is also uncertainty around President Trump's policy on Mexico that could restrict a potential alternative route.

Furthermore, sluggish BEV sales are poised to give rise not only to hybrids, but other types of power as well. E-fuels can emerge as a credible alternative to prolong the use of internal combustion engines, while adoption of hydrogen could accelerate. Highlighting these prospects, auto giant Toyota (7203.jp) has partnered [11] with BMW (BMW.de) for development of fuel cell technology (FCEV).

On the other hand, these adversities may have peaked and 2025 can turn out to be a better year for the industry. Although the election of President Trump in the US casts doubt over the road to net zero, other countries are unlikely to back down and auto electrification seems unstoppable. The European Union has banned sales of diesel and petrol passenger cars and light commercial vehicles from 2035. And despite economic challenges and trade hurdles, China has invested too much to back away from EVs. According the Center for Strategic and International Studies it has spent [12] over $230 billion building the EV industry over the past 15 years. Electric cars, electric batteries and solar energy constitute Beijing's new "three pillars" of growth.

Although uncertainties are likely to persist, with major economies in shaky ground and Trump threatening trade wars, 2025 could offer an improved macroeconomic environment. Price pressures continue to abate and major central banks are bringing interests rates down, helping EV affordability. Chinese authorities are stepping up their stimulus efforts on both the fiscal and monetary front, with their actions starting to bear fruit. The US Fed gears for a shallower and slower easing path in 2025, but strong economy and robust labor market will support spending.

Even if the adoption slowdown persists, the BEV market is still poised for an expansion in 2025. Gartner estimates [13] nearly 61.9 million pure battery electric cars will be on the road representing roughly 35% y/y growth, still substantial, even if not much lower than 2024's 51% increase.

Affordable EV Models:

A Catalyst for Market Growth?

Responding to the diminished BEV appeal, many legacy automakers have backtracked to hybrids. Ford exemplifies this shift and plans to allocate only 30% of annual capex to BEVs (from 40% previously planned), as it Model E segment piles up losses.

Despite the adversities and the strategy shift of many automakers, they still see electrification as the future and look to offer more affordable vehicles. This is the key for mass adoption and the first truly cheap cars could hit the market in 2025. This was after all, part of Elon Musk's original Master Plan [14] from the distant 2006.

Although it looks like the previously mentioned 25K EV may have been sacrificed in favor of autonomy, Tesla still plans to offer "more affordable models", within the first half of 2025. General Motors (GM.us) is set to release [15] the new Chevrolet Bolt before 2025 is out, for less than 30K. Fiat of the Stellantis Group (STLA.fr) - a bona fide hit maker - is poised to launch [16] a fully electric Grande Panda with 2025 and a sub-25K price tag. Volkswagen's 25K ID.2 could come as early as the end of 2025, while orders for the similarly priced retro-futuristic 5 E-Tech from Renault (RNO.fr) are set to begin [17] in January.

Chinese carmakers have a clear competitive edge, with BYD (BYDC.hk) cars starting at around 70K Yuan domestically (roughly 9.2K Euros). Such figures are unlikely to be offered in Europe, but the 20K price tag looks reasonable and BYD already offers models in the 30K price point. More premium EV startups are introducing cheaper spinoff brands, like Xpeng (XPEV.us) and the Mona, with the MO3 exceeding [18] 30,000 deliveries in its first three months.

Autonomous Driving:

The Next Frontier for EVs

Although it feels like we are perpetually on the advent of autonomy, developments could accelerate in 2025 and generate renewed excitement around electro mobility. This is largely due to Elon Musk's push, who has tied Tesla's future to AI and robotics. Although the no-steering wheel/no pedals Cybercab won't arrive until 2026 at best, Mr Musk has promised "fully autonomous unsupervised FSD" existing models in 2025. However, he has been overly optimistic in the past around autonomy and Tesla has a track record of missing deadlines. Regulatory approvals remain a significant hurdle that Mr Musk likely underestimates, but his ties to the Trump administration may expedite this process.

It's not just Tesla that is pushing the full-self driving front, as there are other players that are actually ahead in the race. Alphabet's Waymo already has Level 4 autonomy, with 25 million miles logged [19] through July without a human driver. Over in China, tech giant Baidu (BIDU.hk) appears to be the frontrunner, with the Apollo Go ride hailing service. Its purpose built RT6 has Level 4 autonomy and more the 70% [20] of rides were driverless in the third quarter. Pony.ai which recently debuted in the Nasdaq, has Level 4 and over 39 million km of autonomous driving (with or without driver). BYD has testing permits in China for Level 3 autonomy.

Tesla vs BYD:

Who Will Lead the EV Market in 2025

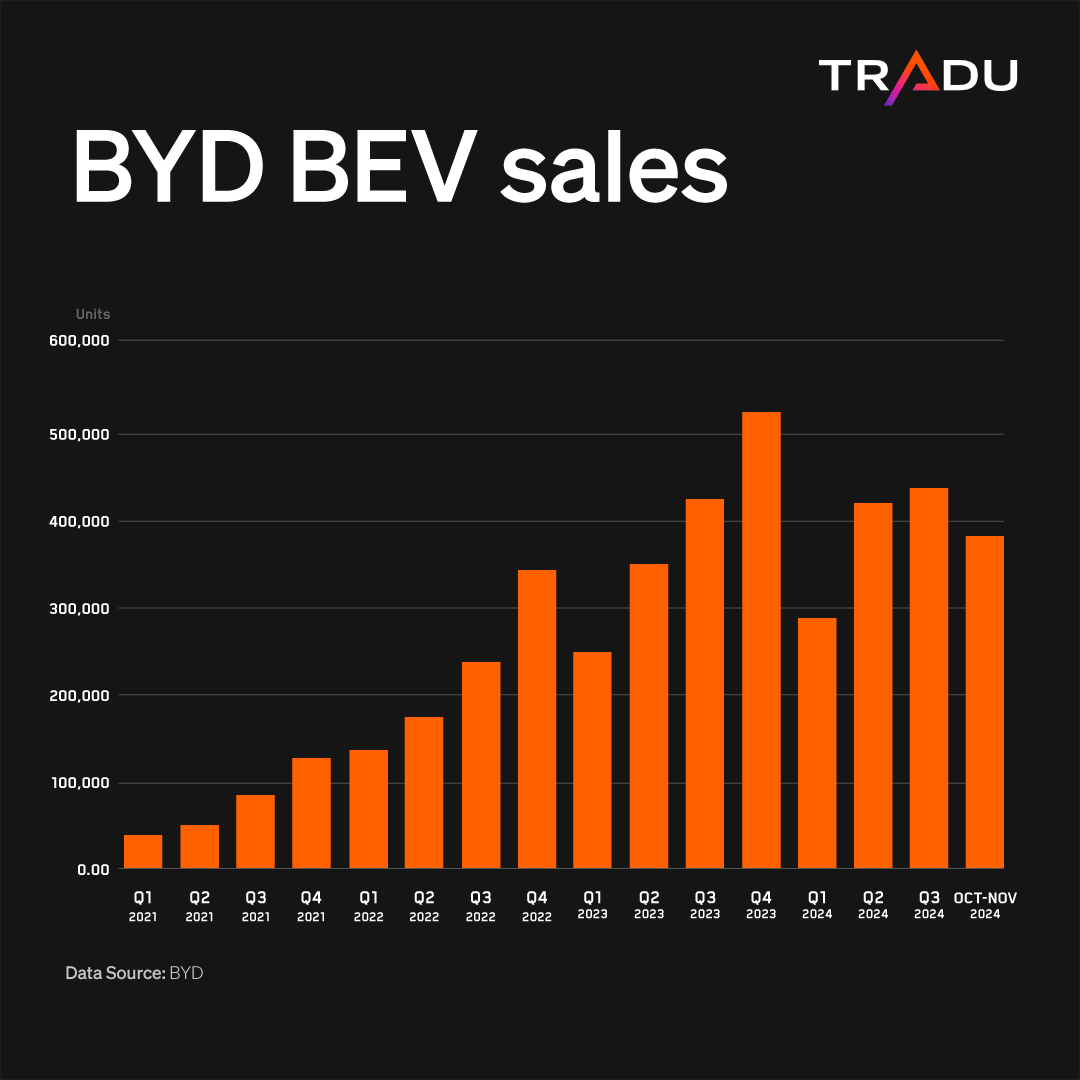

The rivalry between BYD and Tesla is set to remain in the spotlight next year. The Chinese automaker launched its first BEV in 2009, but has managed to dominate sales in a short period of time. It has emerged as the top seller of electrified vehicles in the past two years, but remained below Tesla in pure BEV's at the time of writing. With 1,557,258 deliveries and one month remaining, it has a shot at reaching the top in 2024. Even if it falls short, it will remain a strong contender in 2025.

If Elon Musk's prediction for "20% to 30% vehicle growth" [21], i.e. around 2.2 million cars comes true, it's not going to be easy for the Chinese maker. However, BYD's domestic dominance seems secure, its manufacturing and technological prowess is undisputed, its low entry point gives it a competitive advantage and its global expansion [22] seems unstoppable despite pitfalls from tariffs and trade uncertainty.

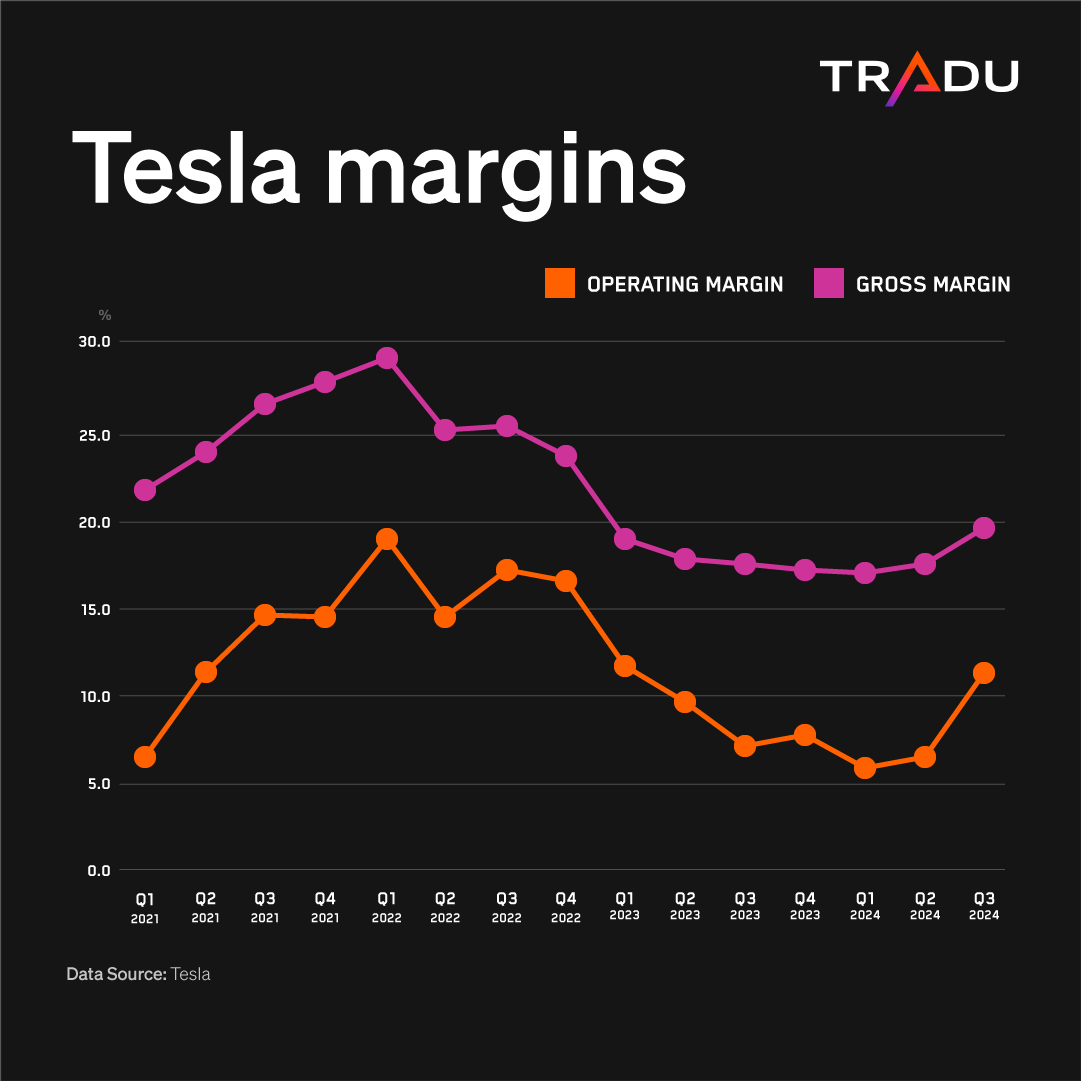

Tesla's automotive business faced significant challenges in 2024, including an unfavorable external environment, growing competition, and an aging lineup. Deliveries are down this year, while days of supply reached historically high levels. Promotional discounts to boost demand hurt profitability despite recent improvement.

However, Tesla is much more than just a car company. Elon Musk has a broader AI vision, with full self-driving and humanoids at its core, which can unlock tremendous value if properly executed. He expects unassisted autonomy next year and although Tesla may actually be behind others, like Waymo, its differentiated approach could give it the lead. It does not rely on expensive Lidar equipment and its solution is not geo-fenced. This means that it can scale better, faster and cheaper, even though it is riskier from a regulatory standpoint.

Tesla's size and margins enable it to withstand persistent challenges far better than legacy automakers, which often incur losses on their electric divisions, and unprofitable startups struggling with funding and scalability. Moreover, the current downturn in EV demand could work in Tesla's favor, as it continues to generate significant revenue from the sale of regulatory credits to traditional manufacturers that fail to meet emission targets.

Xiaomi's EV Journey:

A Smart Ecosystem Vision in Motion

Beyond Tesla and BYD, there are many manufacturers that will be in the spotlight next year. From legacy OEMs like Ford and VW, to startups like Rivian, Nio and Xpeng. However, there is one firm that is particularly intriguing and this is non-other than Xiaomi (XIAO.hk). The Chinese firm is best known as a smartphone giant, ranking third globally in shipments behind Apple and Samsung, according [23] to Canalys. It also offers a diverse range of smart devices, from wearables to home appliances like robot vacuums that provide a huge installed base.

Xiaomi sought to further diversify its portfolio by entering the EV market earlier this year with the launch [24] of the SU7 smart sedan -a move that is neither a gimmick nor a haphazard effort. The company executives envision a highly integrated Human x Car x Home Smart Ecosystem and aspire to position Xiaomi as one of the top five global automakers.

The SU7 is already a success story with demand through the roof. The company expects 130,000 deliveries by the end of 2024, reaching production of 100,000 units in just 230 days - a truly impressive achievement. Given the strong debut, it will be interesting to see how things play out next year. EV sales are likely to more than double in 2025, contributing significantly to Xiaomi's revenues, especially if the rumored second model hits the market. Xiaomi is also advancing in autonomous driving, adopting an AI-driven approach similar to Tesla's for decision making.

Navigating Challenges and Seizing EV Growth Opportunities in 2025

Challenges are expected to persist in the industry with EV demand potentially remaining subdued in 2025. Fresh obstacles could present themselves, with US President Trump exacerbating the slowdown. Existing import tariffs in the US and EU, along with the threat of new trade wars could make it harder for China to channel its overcapacity abroad, but its EV advance seems unstoppable.

On a more optimistic note, the broader macroeconomic environment could improve, especially as major central banks around the world have embarked on monetary easing cycles. The release of cheaper models in 2025 could be the catalyst for the revival of demand, while the push for autonomy could spark renewed enthusiasm.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.