Shares

Netflix resilient amid macro headwinds and Big Tech turmoil, outperforming the struggling Magnificent Seven

Netflix stock is outperforming its Big Tech peers in 2025, standing strong amid market volatility, AI disruption, and Trump-era trade tariffs. As the Magnificent Seven stocks falter, Netflix is behaving more like a consumer staple, emerging as a potential safe haven in a turbulent tech landscape.

Netflix defies the 2025 tech slowdown

Following a strong 2024, Silicon Valley was banking on continued momentum driven by the AI boom and optimism surrounding Trump’s deregulation and tax-cutting agenda. That euphoria, however, quickly faded. Big Tech’s leadership in Artificial Intelligence (AI) is being tested by Chinese rivals offering lower-cost large language models (LLMs), notably following the DeepSeek breakthrough. Meanwhile, Trump’s disruptive trade policies have rekindled fears of both global and domestic recession, dampening US consumer sentiment. Particularly concerning for the tech sector are heightened Sino-US trade tensions and potential new tariffs on semiconductors and electronics.

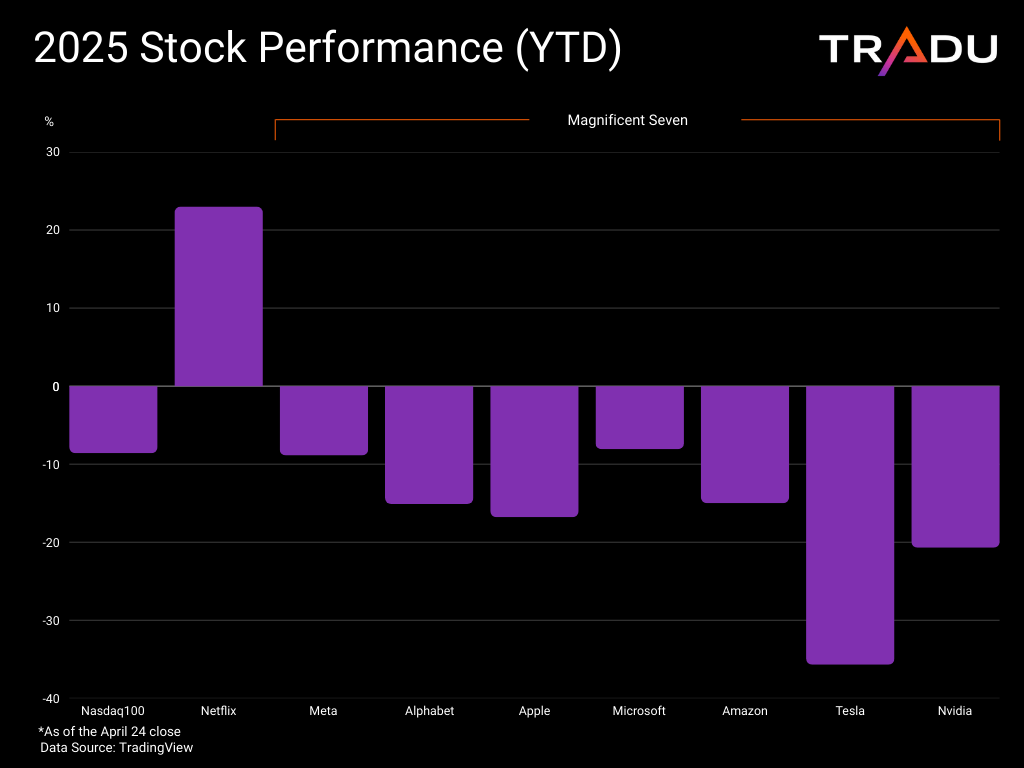

The Magnificent Seven are down this year, reflecting those pressures. Tesla has been hit hardest, with its share price down nearly 36% year-to-date. Kicking off the earnings season for Mag7, it reported poor Q1 results - although Elon Musk’s pledge to spend less time on government (DOGE) work offered the stock a lift. Google-parent Alphabet provided a bright spot with solid results [1], but a slowdown in revenue growth raises concerns. Apple got a temporary relief from a pause in smartphone tariffs, but the US President has signalled more to come. Nvidia faces headwinds from US export controls, expecting a $5.5 billion hit from trade restrictions targeting China. [2]

In stark contrast, Netflix has emerged as a standout performer. Its shares are outpacing the Nasdaq 100 and the broader Magnificent Seven, creating a safe haven narrative during this turbulent period.

Technical indicators point to further Netflix stock gains but hurdles loom

NFLX is up 23% year to date, reaching new record highs in the aftermath of the solid Q1 results and guidance. On the technical front, the Double Bottom formation creates scope for further gains, supported by the strong fundamentals.

However, the elevated valuation can prompt hesitation. Furthermore, the Relative Strength Index enters overbought territory, which could cap the upside and lead to pullbacks, but closes below the EMA200 are needed to negate the bullish momentum.

Source: www.tradingview.com

Why is Netflix outperforming in 2025?

Several factors underpin Netflix’s resilience and make it less exposed to the broader Wall Street downturn. The company’s strong financials and recent upbeat guidance, driven by successful strategic initiatives and its leadership in streaming, are key contributors. Moreover, unlike Apple and other tech heavyweights, Netflix is relatively insulated from tariffs and more resilient in consumer pullbacks.

Resilience in the face of macro adversities

Netflix consolidated its dominance in streaming last year through continued progress on three strategic shifts. First, it successfully implemented a new password-sharing policy, converting many shared users into paying subscribers. Second, it introduced a lower-cost, ad-supported tier, offering a more accessible entry point. Third, it entered the live sports arena - highlighted by two NFL Christmas Day games - which has become an increasingly vital content segment.

The high-stakes business changes worked out really well, driving growth in the streamers user base. While Netflix no longer reports subscriber numbers, during the last earnings call executives cited over $300 million paid households, representing an audience of over 700 million people. Yet, they view this as a small proportion of their addressable market, with still “hundreds of millions of folks to sign up”. [3]

Its robust content slate across many regions, the inclusion of sports that can enhance engagement and draw wider audiences, and the attractive entry point turn Netflix into a streaming imperative. The dominant position makes the company look almost like a consumer staple, shielding it against prospects of economic downturn and pullbacks in household spending. Co-CEO Greg Peters expressed confidence amid economic uncertainty, stating there’s “nothing really significant to note” in terms of macro impact, and voiced optimism that demand for entertainment will stay “strong”.

Blockbuster earnings and guidance

Netflix’s strategic pivot has not only expanded its audience but also strengthened its financials. The crackdown on password sharing has boosted revenues from higher subscriptions, the ad-supported tier opened a new stream, while live sports are crucial in this shift.

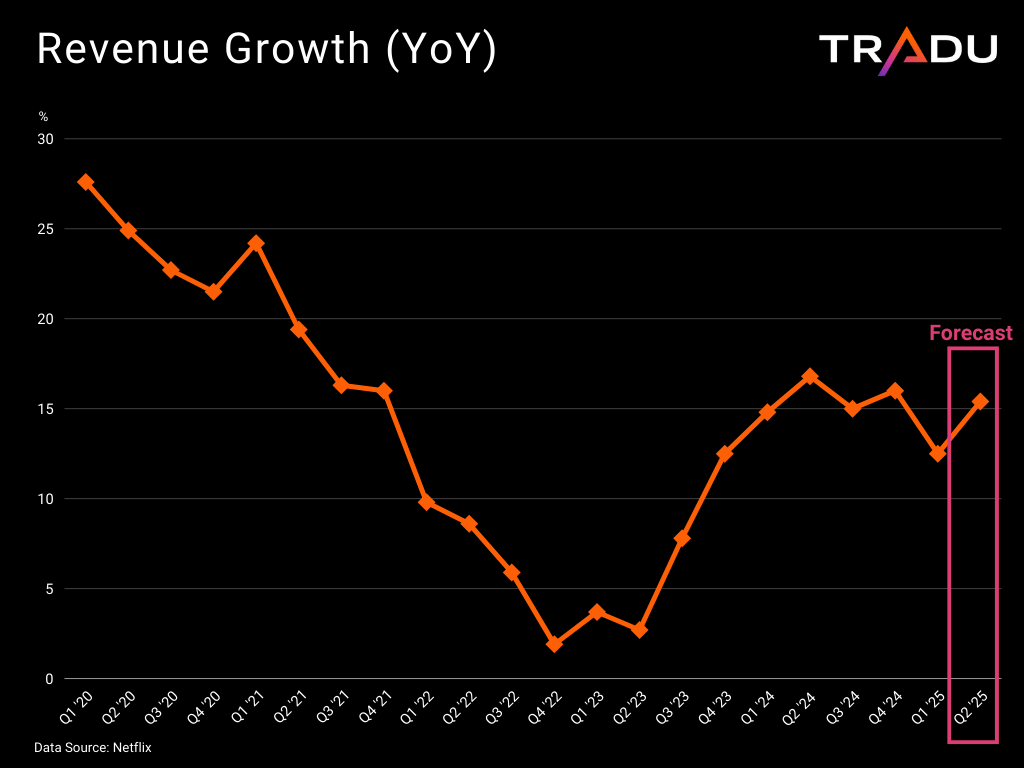

Building on momentum from 2024, the company delivered record-breaking Q1 2025 results [4]. Revenues reached new all-time highs of $10.543 billion, even though growth slowed. Its bottom lines also impressed, as net income jumped 23.9%, to a record of $2.89 billion.

This strong financial position and its streaming leadership place Netflix in solid ground to navigate the current turbulent period. Executives offered upbeat guidance, expecting new record top and bottom lines, and acceleration in the pace of growth.

Netflix is not immune to challenges

Despite this year’s strong showing, Netflix is not invulnerable to macro headwinds and the advancements of competitors. The boost from password-sharing changes is likely to diminish over time, as evidenced by the slowdown in revenue growth since its Q2 2024 peak.

Although Netflix is the streaming leader, rivals like Disney are making strides and offer compelling content, while the popularity of free platform (known as FAST) is rising. Furthermore, Netflix’s limited sports offering - compared to more comprehensive rivals - could weaken its position if budget-conscious consumers reduce subscriptions.

Even if Netflix avoids major user churn, it is not immune to a global economic downtrend. Such outcome could curtail advertising spending and hurt the company’s efforts to generate more revenues from commercials. Despite its streaming dominance, Netflix remains a small player in the wider media landscape and its limited sports exposure makes it vulnerable to spending pullbacks in advertising. Nielsen’s media distributor gauge shows that Netflix fights for just the fifth place of TV viewership in the US, with the top spots consistently occupied by YouTube and legacy media giants like Disney. [5]

Positioned to weather challenges but not bulletproof

Netflix has proven its resilience during a turbulent year for Big Tech. Its smart business strategy, record-breaking financials, and limited exposure to trade tariffs have allowed it to outperform the Magnificent Seven and navigate macroeconomic uncertainty.

Still, it's not bulletproof. Growth may slow, and macro conditions could test the strength of its newer revenue models like advertising. Yet with a dominant market position, a broad global audience, and an evolving content mix, Netflix is well-positioned to weather whatever comes next.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.