Shares

Tesla caught between Robotaxi ambitions and EV struggles ahead of Q2 2025 earnings

Shares of Tesla have declined year-to-date amid ongoing challenges in its core automotive business—pressures that could persist into Q2 2025, as falling electric vehicle (EV) deliveries are likely to weigh on both revenue and profitability. Investor focus will also centre on updates regarding Tesla’s long-promised affordable EV, seen as key to reviving sales, as well as progress on its robotaxi strategy. Although Tesla officially launched its robotaxi service last month, the rollout has been limited and cautious, fuelling concerns over scalability and readiness for broader deployment.

Weak EV demand, deteriorating financials, and autonomous driving push

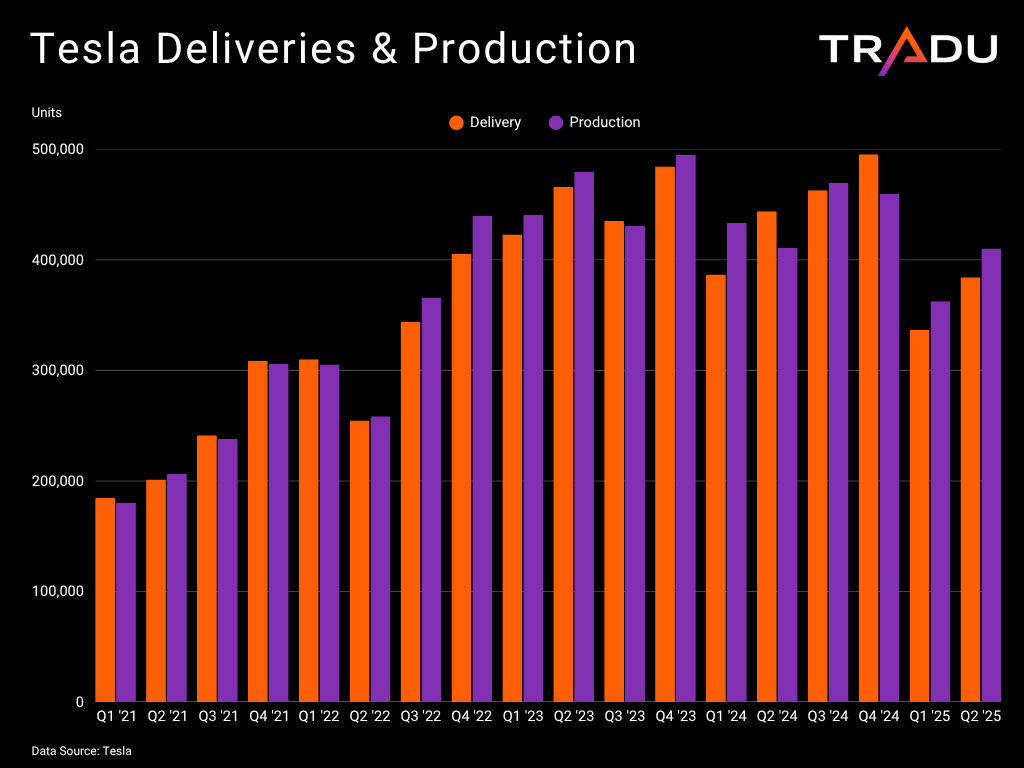

Tesla is navigating a challenging period amid a tough external environment, unfavourable shifts in US clean energy policies, Elon Musk’s political entanglements, an ageing vehicle line-up, and intensifying competition. These factors have contributed to weakening demand for Tesla’s EVs, with deliveries dropping 13.5% y/y in the second quarter [1].

This raises the risk of a second straight annual contraction and also allowed China’s BYD to surpass Tesla for a second straight quarter in pure BEV sales. Meanwhile, Xiaomi is also posing a threat - its Model Y rival, the YU7, received 289,000 orders within just the first hour of launch [2]. European legacy automakers are gaining ground too, focusing on cheaper EVs like the FIAT Panda and Renault 5, both of which are already on the market.

Although Elon Musk has promised a more affordable vehicle, the details and timeline remain vague. Rather than introducing an all-new model, Tesla may instead release lower-cost variants of existing vehicles. During the last earnings call, VP of Vehicle Engineering Lars Moravy stated that upcoming models will “resemble, in form and shape, the cars we currently make”. [3]

The drop in sales is expected to weigh on both revenue and profitability in the second-quarter results. If such outcome materializes, it would mark a continuation of a downward trend: overall revenue declined 9% year-on-year in Q1, while both operating and gross margins were at their lowest levels since Q2 2019. [4]

Tesla’s diminished appeal and weakening financials have directly impacted its stock. TSLA is down nearly 20% year-to-date, making it the worst performer among the Magnificent Seven tech stocks and missing out on the broader market rally. However, the stock runs a profitable month and maintains a bullish bias above the EMA200, keeping the path towards new all-time highs open.

Source: www.tradingview.com

Despite the challenging backdrop, there are reasons for optimism. Tesla has updated its best-selling Model Y, which could help revive demand. Additionally, the planned elimination of the $7,500 tax credit for new EV purchases in September under the One Big Beautiful Bill could trigger a short-term boost in sales. In the longer term, Tesla may emerge as a relative beneficiary of regulatory changes and Trump’s tariffs, thanks to its localised production, strong margins, and dominant US market share.

Crucially, Elon Musk is shifting Tesla’s focus towards AI, humanoid robots, and autonomous driving. While the purpose-built Cybercab is slated for volume production in 2026, Tesla launched its robotaxi service in Austin last month [5]. This marks a significant milestone in Musk’s self-driving vision, which - if successfully executed - could unlock substantial value.

Unlike other autonomous ride-hailing firms, Tesla avoids using costly LiDAR equipment, relying instead on cameras and AI. This approach allows for faster scalability at a significantly lower cost. However, it also raises concerns over safety and performance, with several online videos highlighting errors by Tesla’s robotaxi fleet. Tesla is far behind rivals like Waymo and fast expansion may depend on a lenient regulatory environment, and Musk’s recent feud with President Trump casts doubt on whether policies supportive of autonomous driving will materialise.

As Tesla delivers its second quarter earnings on Wednesday July 23, there are three key areas in focus.

- Financial performance, which may continue to deteriorate following the sharp decline in sales.

- Updates on the affordable vehicle, which could rejuvenate demand and counter rising competition.

- Progress on the robotaxi rollout, which represents a high-stakes pivot into autonomous services.

Any encouraging news on the robotaxi could help investors look past the automotive struggles and focus on Tesla's long-term transformation.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.