Shares

Tesla Q2 2025 earnings: Elon Musk focuses on Robotaxi as EV struggles persist

Tesla’s revenue and profits fell in Q2, as reported in Thursday’s earnings release, driven by declining EV deliveries amid weakening consumer demand and rising competition from BYD and other rivals. Trump’s tariffs and shifting US clean energy policies may further pressure growth. However, Tesla is now focusing on more affordable electric vehicles to revive demand, while CEO Elon Musk is pushing ahead with the company’s high-stakes vision: the Robotaxi, a service that could unlock significant value if successfully executed.

Tesla grapples with weak EV appeal

Tesla is navigating a challenging period. President Trump’s tariffs have created an uncertain macroeconomic backdrop, while the rollback of EV incentives under the One Big Beautiful Bill (OBBB) could further dampen adoption. Compounding these external headwinds are Tesla’s own missteps - including Elon Musk’s political entanglements, strategic errors, and intensifying competition.

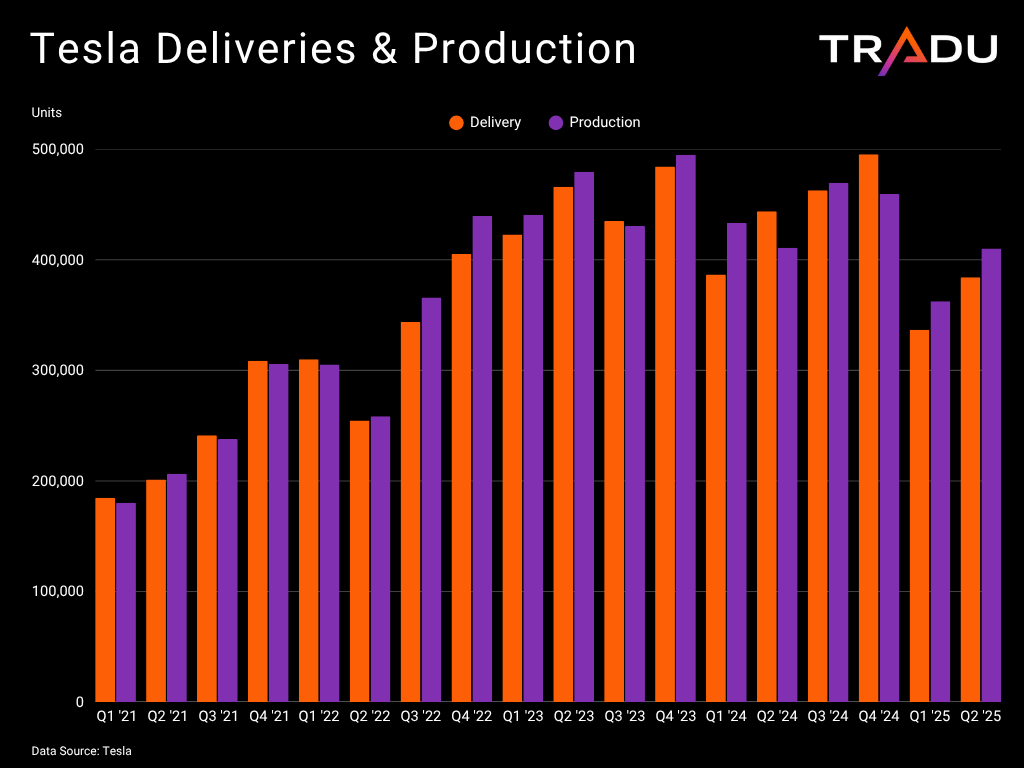

Musk’s political affiliations have damaged the brand’s appeal, particularly in Democratic-leaning and EV-forward states like California. According to the California New Car Dealers Association, Tesla sales fell for a seventh consecutive quarter in Q2 [1]. A similar pattern has emerged in Europe, where YouGov polls show a decline in brand favourability in key countries [2], [3]. Tesla’s sales in the EU, EFTA, and UK fell by 33.2% in the first half of the year, despite an increase in overall BEV registrations, according to the European Automobile Manufacturers’ Association (ACEA). [4]

Tesla has an aging line up as its latest truly new model is the Cybertruck, which is on the market for almost two years. Despite its futuristic design and initial buzz, the Cybertruck has proven a strategic misstep. It was never intended for mass production like the Model Y, its polarising design has limited appeal, and sales have lagged. Underscoring this underperformance, the Cybertruck was outsold by the niche GMC Hummer in Q2, according to Cox Automotive. [5]

Meanwhile, competition is intensifying. New entrants and established automakers are expanding line-ups, improving affordability, and leveraging technological advancements to accelerate EV uptake. Chinese giant BYD surpassed Tesla in BEV deliveries in Q2, maintaining dominance in China while advancing in Europe. Xiaomi’s YU7 SUV, priced below the Model Y, drew 289,000 orders in its first hour of is launch [6]. European legacy automakers are also gaining ground, with affordable EVs such as the Fiat Panda and Renault E5 hitting the market.

These challenges led to a 13.5% drop in deliveries during Q2, raising the risk of a second consecutive annual decline in 2025. However, sales improved on a sequential basis, aided by the refreshed Model Y - a possible sign of stabilisation. Additionally, the end of US tax incentives may provide a near-term boost, with Tesla potentially less exposed than rivals due to its dominant market position.

Low EV demand weighs on financials

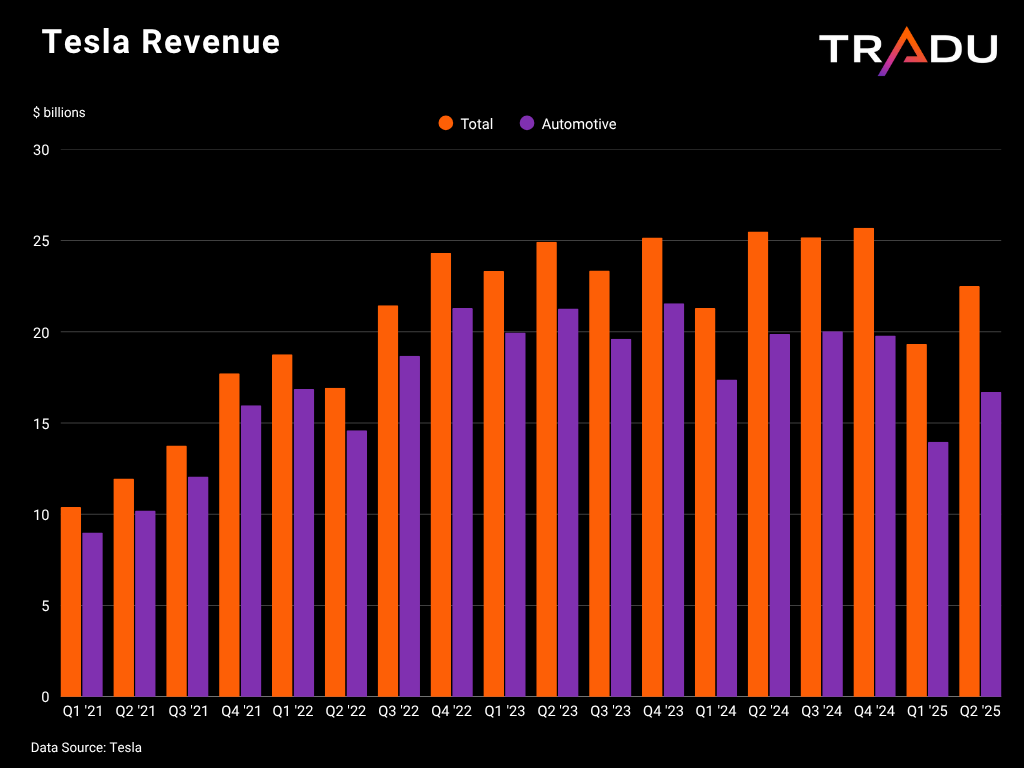

Sluggish demand and ongoing promotions to support sales have continued to impact Tesla’s financial performance. Revenue fell 12% year-on-year in Q2 - the sharpest decline since Q3 2012 - while operating income dropped 42% to $923 million, compressing the operating margin to 4.1%. [7]

Further deterioration is possible, with CEO Elon Musk saying that “we probably could have a few rough quarters” during the earnings calls [8]. Trade uncertainty stemming from Trump’s tariffs and shifts in clean energy policies are taking a toll. Tesla’s CFO highlighted the impact of tariffs on profitability and flagged that OBBB was dampening both vehicle sales and sales of regulatory credits to other OEMs.

Nevertheless, Tesla may benefit from these policy shifts relative to peers, thanks to its strong domestic production base, healthy margins, and dominant US market share. Financials also improved sequentially, offering a reasons for optimism.

Affordable EVs and Robotaxi vision

To reignite demand and fend off growing competition, Tesla needs to bring more affordable vehicles to market. The price premium on EVs remains a barrier, especially in today’s uncertain economic climate. The company has started production of a more accessible model, but availability isn’t expected until Q4, according to VP of Vehicle Engineering Lars Moravy.

Details remain vague, and Tesla appears to have moved away from launching an entirely new 25K model. Instead, the firm is likely preparing variations of its existing vehicles. Moravy hinted at this during the previous earnings call [9], stating that upcoming models will “resemble, in form and shape, the cars we currently make”. In any case, Tesla is late to the party. Competitors already offer EVs in the 20-25K range, and Tesla will struggle to match the lowest prices, especially in China.

Regardless, Tesla executives spent little time discussing affordable vehicles during the call, focusing instead on the company’s bold bet: the Robotaxi. The service launched in Austin last month, with Musk anticipating rapid expansion “despite teething pains”. He anticipates expansion to more regions and “probably addressing” half of the US population by the end of 2025 – pending regulatory approvals. Volume production of the purpose-built Cybercab is slated for 2026, at which point owners will also be able to add their vehicles to the autonomous fleet.

These are undoubtedly ambitious goals. Tesla’s self-driving approach - relying solely on cameras and AI, without LiDAR - can scale faster and at lower cost. However, it also raises safety concerns and regulatory challenges, which the CEO may be underestimating, Concrete details on progress remain limited, while the robotaxi launch was limited and bumby. Moreover, Tesla still trails established players like Waymo in this space.

Tesla stock caught between AI hopes and EV weakness

Tesla is in a transitional phase. Its core automotive business continues to struggle, while its self-driving ambitions have yet to materialise at scale. Weak EV demand, a challenging policy environment, and Musk’s public clashes with President Trump are exacerbating adversities.

Reflecting these challenges, Tesla shares have declined in 2025, underperforming both the broader market and its Magnificent Seven tech peers. Headwinds could persist, keeping the stock vulnerable to further downside.

On the upside, Tesla’s Robotaxi programme and humanoid robot projects offer longer-term promise. Progress in these areas could support investor sentiment and the srock. Additionally, sales appear to be stabilising, and the refreshed Model Y - along with the eventual arrival of a more affordable model - may help revive demand.

Source: www.tradingview.com

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.