Paradigm shift in defence spending amid heightened geopolitical uncertainty

The return of Donald Trump to the White House is disrupting the global economic and geopolitical landscape. He is introducing trade tariffs on traditional US allies while pressuring NATO members to increase their defence spending. At the same time, he has expressed interest in gaining control of Greenland and Panama - without [1] ruling out military force - and has repeatedly suggested [2] that Canada should become the US’s "Fifty-First State". His stance on the Ukraine-Russia conflict is causing concern in Europe, while hostilities in the Middle East persist despite his stated aim of ending both wars.

Against this backdrop of geopolitical uncertainty and rising tensions, the European Union is embarking on a significant rearmament effort, marking a paradigm shift in defence policy. The European Commission aims [3] to mobilise nearly €800 billion over the next four years, while the German Parliament has voted [4] to reform the country's debt brake to facilitate higher military spending. In the UK, Prime Minister Starmer has committed [5] to increasing military spending to 2.5% of GDP by 2027, with a further target of 3% in the next Parliament. These measures can not only revitalise Europe's struggling economies but also spark a defence spending supercycle. European contractors expect strong demand, with their stock prices surging this year.

Meanwhile, US Arms manufacturers face a more complicated environment, as this rearmament could redirect funding towards European contractors at the expense of American firms. Moreover, the President’s isolationist approach, combined with the work of the Musk-led Department of Energy Efficiency (DOGE) create ambiguity around the country’s defence budget. Defence Secretary Hegseth recently announced [6] further spending cuts, bringing total savings to $800 million. Although this is a considerable sum, it represents only a small fraction of the $850 billion budget and is unlikely to significantly impact US military capabilities.

Any meaningful cuts will be challenging given the current security environment, increasing spending from China [7] and shifting trends in the age of Artificial Intelligence. In a recent Fox News interview, President Trump expressed support for defence cuts but stated [8], "not now because you have China, you have Russia, you have a lot of problems out there." He has also pledged [9] to build "the most powerful military of the future" and a US-made, "state-of-the-art Golden Dome missile defence shield".

These developments suggest that high levels of defence spending will persist, but this is not guaranteed. A halt of strikes in energy infrastructure from Russia[10] and Ukraine [11] helps the case for a ceasefire and, eventually, a resolution to the war. There is also hope for a similar outcome in the Middle East, even if the bar is high in both cases. Additionally, while the EU is prepared for bolder action, it still faces a fragmented defence industry and diverging priorities among member states.

As geopolitical tensions continue, the defence sector will remain in focus throughout the second quarter. European arms manufacturers such as Rheinmetall, BAE Systems, and Leonardo stand to benefit from the ReArm Europe initiative, while US giants Lockheed Martin and RTX are well positioned to capitalise on the Golden Dome ambitions.

Rheinmetall: On solid footing to benefit from Germany’s spending

The Germany-based arms manufacturer produces a wide range of military equipment, including armoured vehicles, artillery, ammunition, and electronic solutions. With offices and production sites in more than 30 countries, the company employs over 31,000 people.

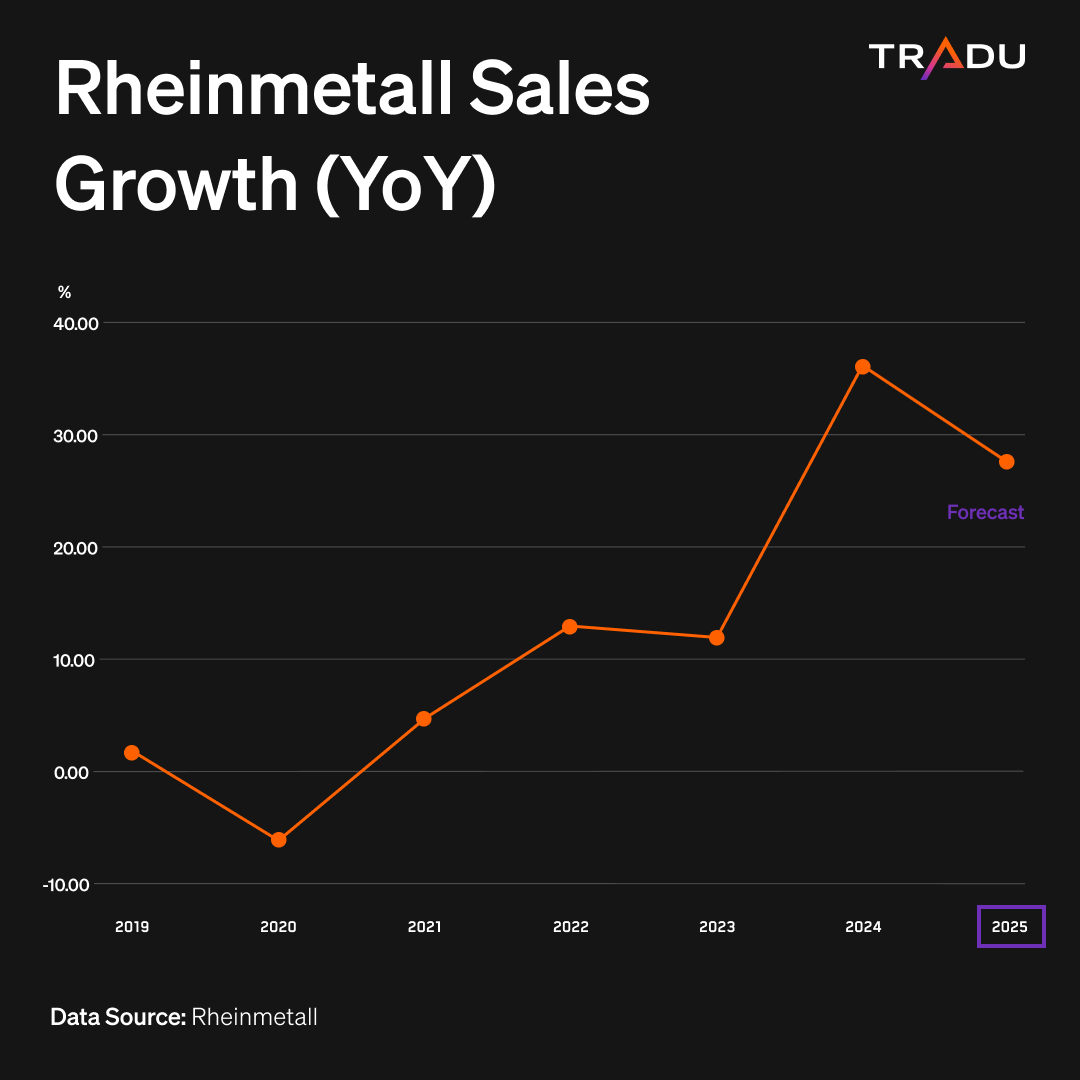

The war in Ukraine has significantly boosted Rheinmetall’s business, particularly in its Weapons and Ammunition segment, which has higher margins and is easier to ramp up to meet demand. In 2024, sales jumped [12] 58% year-on-year, with operating profit nearly doubling - outpacing growth in its larger Vehicle Systems division. Total sales increased 36% to €9.75 billion, while operating income climbed 61%.

Rheinmetall is well positioned to benefit from Europe’s rearmament efforts and ongoing geopolitical uncertainty. In the company’s full-year results announcement, the CEO described growth prospects as something "we have never experienced before". Management also reported a record order backlog of €55 billion and expects sales to continue expanding at a robust 25%-30% pace this year, alongside improving operating margins.

Despite strong prospects, challenges remain, particularly if the war in Ukraine comes to an end, which could slow demand. Additionally, Rheinmetall has ramped up capital expenditures in recent years to accommodate rising orders, but further investment is needed to expand production capacity.

The company’s market capitalisation now matches that of Volkswagen, Germany’s largest automaker, underscoring the growing appeal of European defence stocks. Rheinmetall’s meteoric rise has continued into 2025, with new record highs driven by sustained demand. However, high valuations could present headwinds going forward.

Source: www.tradingview.com

BAE Systems: Scale brings both opportunities and challenges

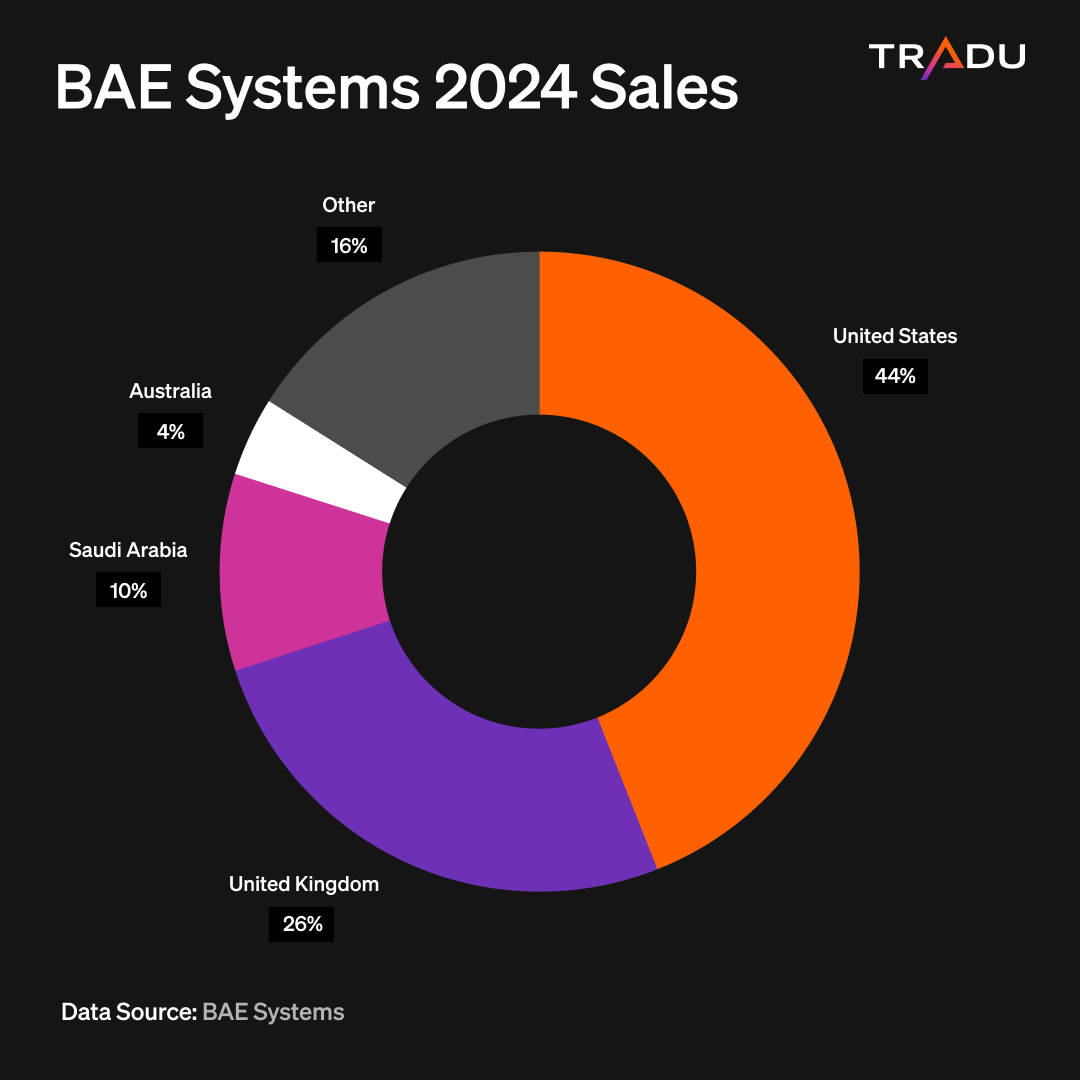

The British company is one of Europe's largest defence contractors and ranks among the top globally, according to the 2023 classification [13] by the Stockholm International Peace Research Institute (SIPRI). With over 100,000 employees across 40 countries, it is involved in the design and manufacturing of military aircrafts, ships, submarines, ammunition, combat vehicles, and more.

Its magnitude and diverse product range have positioned BAE Systems to capitalise on the geopolitical unrest of recent years. In 2024, sales growth accelerated [14] by 14% to £28.34 billion, while its order backlog reached an all-time high. The company also increased capital expenditures to expand production capacity and expects further sales growth this year. Its CEO is “confident in the positive momentum of our business into the future”.

Nonetheless, there are reasons for caution. A decline in order intake last year raises concerns, while the company’s 2025 sales growth projection of 7%-9% is far from impressive and would mark a slowdown. Additionally, the firm’s global presence could become a liability in a second Trump 2.0 era. With the United States accounting for the majority of its sales, the company may face challenges from Trump's protectionist policies and disruptive trade agenda.

After a lacklustre 2024, BAE Systems’ shares (BA) have regained momentum in 2025, reaching fresh record highs. While the broader defence spending surge could drive further upside, underwhelming guidance and geopolitical risks may limit gains and trigger potential pullbacks.

Source: www.tradingview.com

Leonardo: Deep reach and R&D commitment

The Italian-based firm is among Europe’s largest contractors, operating in 150 countries worldwide. It has an industrial presence in key markets such as the United States and the United Kingdom, with a workforce exceeding 60,000 employees. The company is involved in a broad range of military projects, including helicopters, drones, and electronic systems.

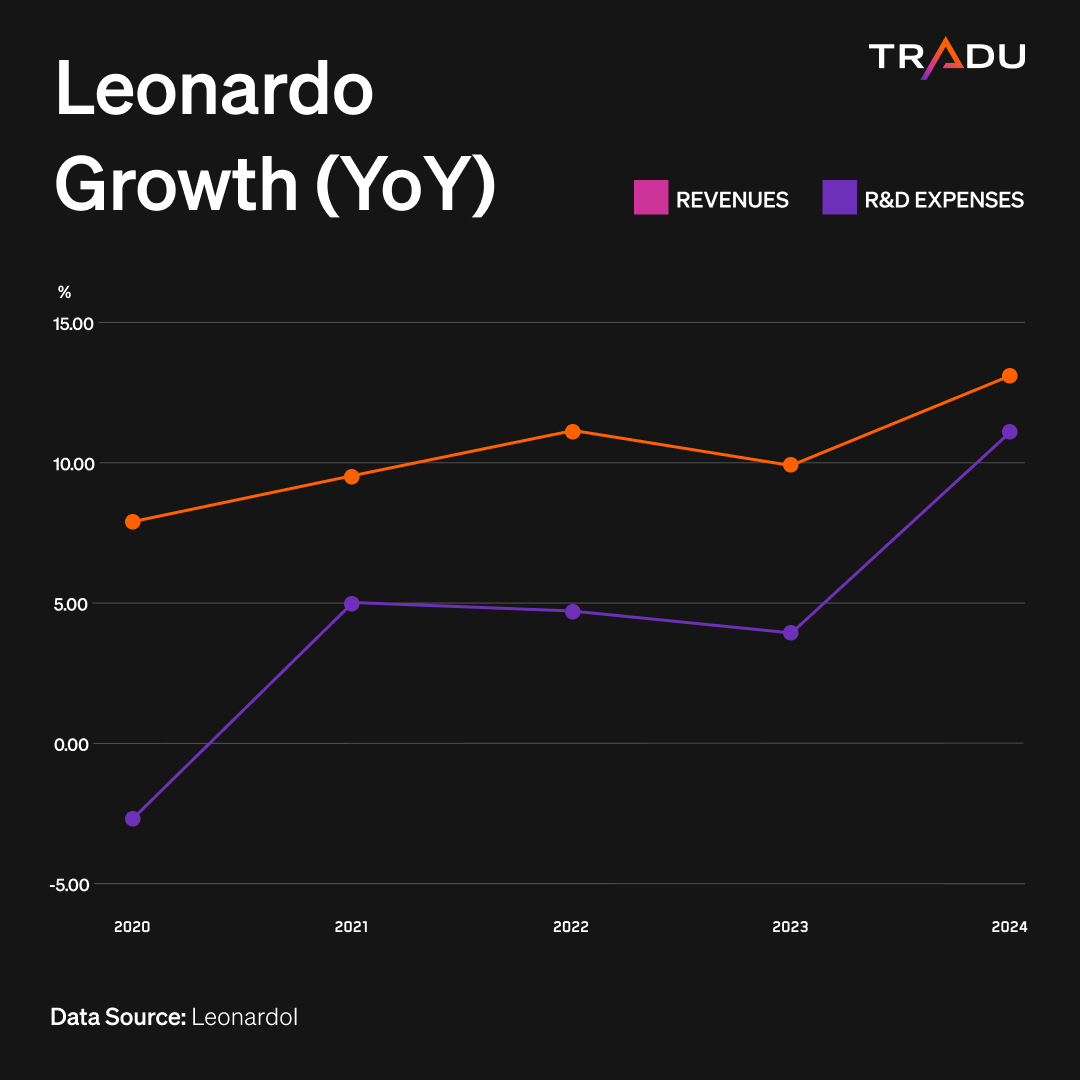

Leonardo's global reach and strong investment in Research & Development (R&D) give it an edge. The company’s R&D spending has consistently grown at a faster rate than sales, enabling it to capitalise on Europe’s rearmament plans and adapt to evolving military trends. In 2024, revenues grew [15] by 11.1% to €17.8 billion, while its order backlog surpassed €44 billion. Management has strong visibility, offering guidance through to 2028, expecting [16] cumulative revenues to grow at CAGR of 6%.

However, this outlook appears somewhat conservative, and Leonardo’s relatively low profit margins remain a concern. Additionally, its emphasis on alliances and partnerships may present challenges in Europe’s still-fragmented defence sector, especially amid rising protectionist policies under the second Trump presidency.

Shares of Leonardo (LDO) have now entered their fifth consecutive year of growth, with a strong rally to record highs. While Europe’s defence spending boom could sustain further gains, this year’s rapid surge raises valuation concerns and creates risk of a market correction.

Source: www.tradingview.com

Lockheed Martin: Well-positioned for supercycle windfall, but pitfalls loom

Lockheed Martin, the world's largest defence company according to SIPRI, operates over 350 facilities worldwide and employs more than 120,000 people. Its extensive portfolio includes high-profile products such as the F-35 fighter jet, Sikorsky helicopters, Javelin portable missile systems, and the Aegis naval combat system.

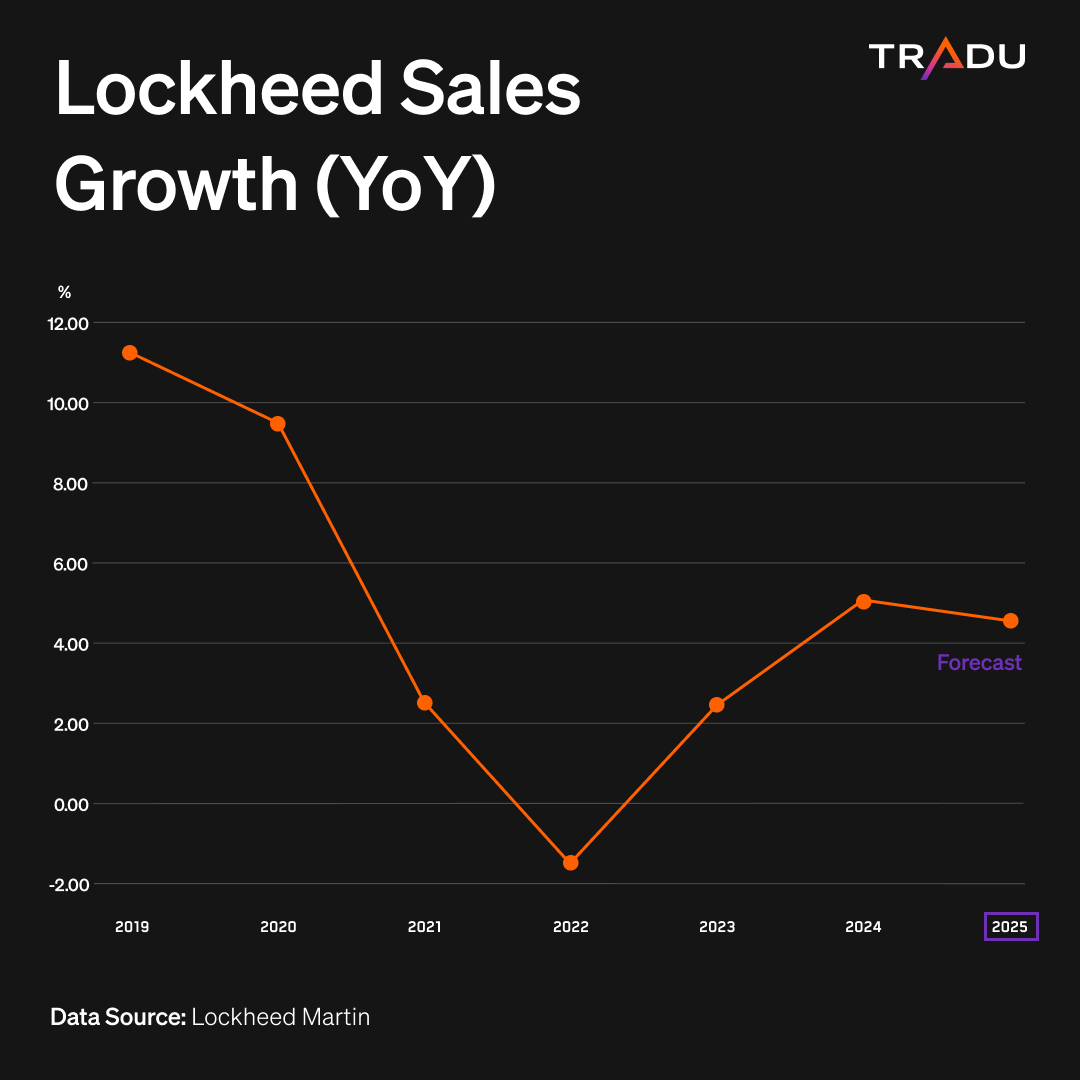

The US defence giant had a strong 2024, with sales rising 4% to $71 billion and a record backlog of $176 billion. Its CEO spoke [17] of “another successful and productive year”. Lockheed Martin’s global reach places it in a strong position to capitalise on heightened geopolitical tensions and President Trump’s military plans.

However, its sales growth lags behind European rivals, and management expects it to remain at similar levels this year. Additionally, net earnings declined, impacted by losses in classified programmes, painting a mixed financial picture.

The firm also faces challenges from rifts between the United States and its allies amid protectionist forces. The European Union looks to boost its own capabilities, while neighboring Canada is reexamining [18] its multi-billion commitment to buy 88 of Lockheed’s F-35s, in response to Trump’s tariffs.

Shares of Lockheed Martin (LMT) performed well in 2024, reaching all-time highs. However, the stock has since pulled back, and 2025 has started with losses, raising the risk of further declines.

Source: www.tradingview.com

RTX: Holding a strong hand in an uncertain environment

RTX stands among the world’s top aerospace and defence giants, renowned for its missile systems like the Patriot, alongside a broad portfolio that includes radars, jet engines (via Pratt & Whitney), and electronic warfare solutions. With over 185,000 employees and a global manufacturing footprint, RTX wields significant influence in the industry.

The company delivered robust 2024 results [19], with adjusted sales rising 9% year-on-year to $80.7 billion and adjusted earnings per share (EPS) picked up pace with a 13% increase, with its CEO touting “unprecedented demand”. Crucially, RTX’s sizable defence and overall order backlog continued to increase, providing solid ground for further strength. Furthermore, its work on Israel’s Iron Dome [20] may give it an edge in President Trump’s Golden Dome initiative.

Yet, challenges loom. RTX forecasts a slower organic revenue growth of 4%-6% for 2025, with EPS projections of $6.00-$6.15, raising concerns about profitability momentum. Additionally, Boeing’s lingering struggles could create turbulence for RTX, despite the resumption of avionics purchase orders, as noted in its last earnings call.

The stock had a blockbuster first quarter, with continued geopolitical uncertainty supporting further advances. On the other hand, slowing sales and EU’s efforts to boost its own defence industry can create headwinds.

Source: www.tradingview.com

Defence supercycle on the horizon, but not a fait accompli

Escalating trade tensions, rising protectionism, fraught Sino-Western relations, and ongoing conflicts in Ukraine and the Middle East, combined with the military implications of AI breakthroughs, are fuelling calls for greater investments. With the EU unveiling massive rearmament plans and the US pursuing its Golden Dome missile defence initiative, we could be on the precipice of a defence supercycle - one that may continue to turbocharge the financials and stock performance of arms manufacturers.

However, obstacles remain. Trump’s isolationist leanings, his stated ambition to end major ongoing wars, and his broader push for government efficiency could curtail defence spending. Meanwhile, despite the EU’s ambitious commitments, execution could prove slow and complex.

With defence stocks already rallying sharply this year - particularly in Europe - concerns over valuations and what is already priced in may begin to surface. While the conditions for a prolonged boom are aligning, the defence supercycle is not guaranteed.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.