Forex

Central Banks: Divergent Monetary Paths Set the Stage for Market Volatility in 2025

Paradigm Shift: Pivot to Easing, but Without Cohesion

In response to the inflation surge fueled by pandemic stimulus, central banks tightened aggressively in recent years and kept rates high for a long time, to ensure they brought prices under control. However, as pressures abated, major central banks pivoted to less restrictive settings this year, initiating interest rate reductions.

Even though looser monetary policies found broad adoption around the world, cohesion remained elusive. Each institution responded to its unique set of challenges, implementing varying degrees of easing at its own pace. Extrapolating the divergence, some key banks refrained from cutting rates entirely, whereas others moved in the opposite direction, opting to hike rates instead.

Central banks of the G-10 economies perfectly illustrate the uneven nature of this endeavor. The most dovish among them is the Bank of Canada, which has delivered 175 basis points (bps) of easing this year, including some outsized moves. At the opposite end of the spectrum, the Bank of Japan raised rates by 50 bps. Other prominent easing frontrunners include Sweden’s Riksbank (150 bps) and Switzerland’s SNB (125 bps). Meanwhile, the Bank of England has adopted a more cautious path, the ECB picks up speed and the Fed turns reticent after September’s jumbo pivot. Outside the G-10, Australia’s RBA and India’s RBI are among the notable holdouts since they have refrained from lowering rates.

Looking ahead, monetary policy ambivalence will persist, and the landscape could become even murkier. Trump’s return to the White House can heighten macroeconomic uncertainty, complicating the task for central banks. Against this backdrop, the US Fed, the European Central Bank, the Reserve Bank of Australia, the Reserve Bank of India, and the Bank of Japan are going to be among the most interesting players to monitor in the coming months.

Complex Macros: Trump’s Return Could Heighten Uncertainty

Central banks face the challenging task of navigating a highly uncertain macroeconomic environment, and the return of Donald Trump to the White House could make their work even more difficult. His plans can inject renewed vigor into the already strong US economy, as his platform [1] calls for deregulation and tax cuts, which can spur economic activity. However, such a stimulus may come with side effects, particularly reflationary pressures. If prices flare up again, the Fed may be forced to implement a shallow easing path, just months after its forceful pivot.

While optimism abounds among market participants, a positive economic outcome is far from guaranteed. His policies could add [2]trillions of dollars to the US debt, while tighter immigration and protectionist policies can sap consumer spending and harm the economy. If this scenario were to materialize, the Fed would need to adopt a different playbook to address the fallout.

The implications of a second Trump Presidency extend beyond the United States, further complicating the operating environment of central banks around the world. His threat [3]of sweeping tariffs - up to 60% for China and 20% on other trading partner - will disrupt trade, increase product prices, and create economic headwinds. Emerging economies could be particularly exposed, leaving their central banks with tough choices. Aggressive easing would help counter the negative impact of tariffs, but the resulting currency depreciations could bring their own set of challenges, like higher costs and capital outflows. It is not just emerging markets that are at risk though. Advanced economies would not be immune either. For instance, the European Union—already grappling with economic fragility—could face an even greater downturn as protectionist measures stifle trade and growth.

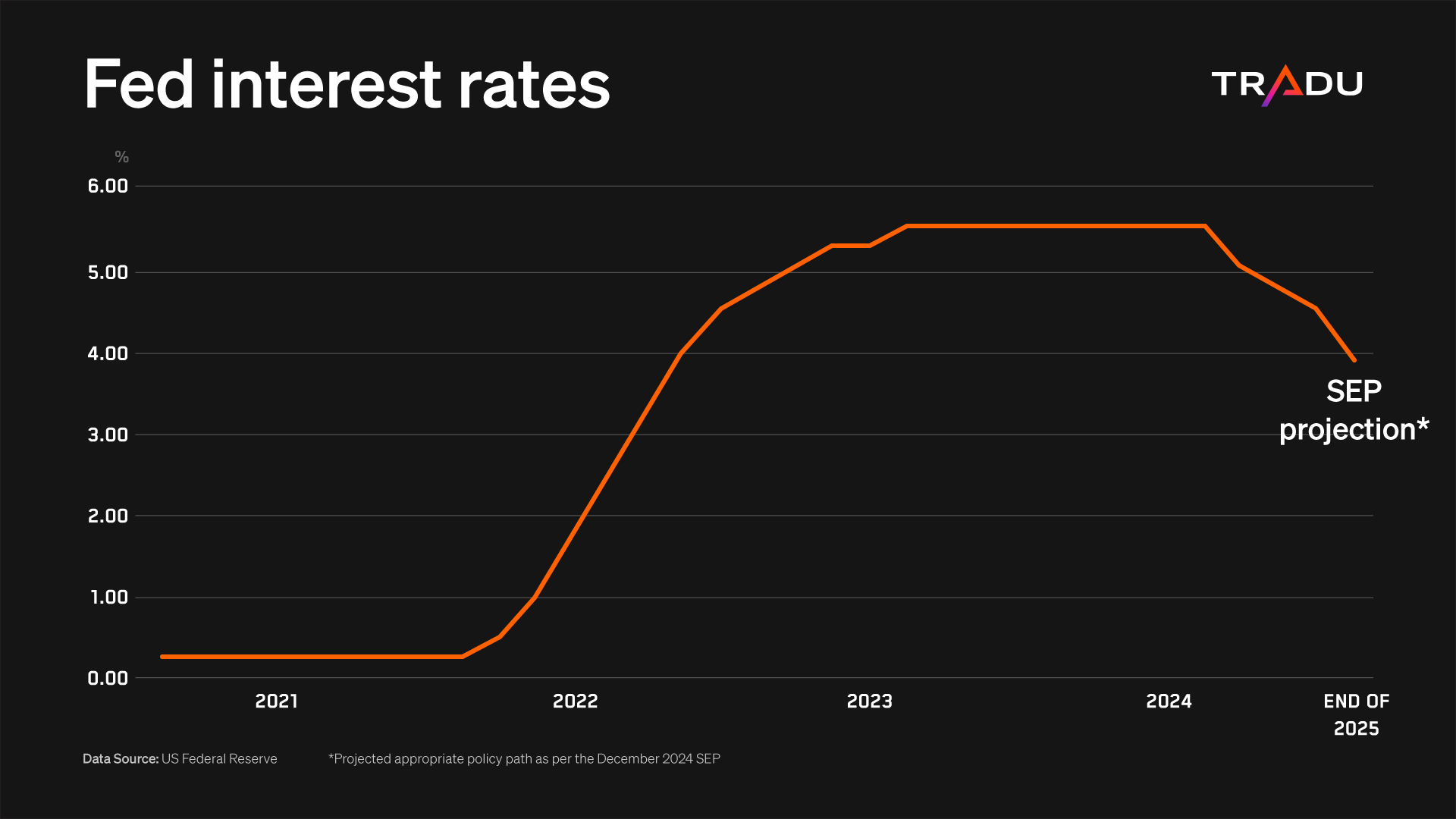

US Fed: On Track for Fewer Cuts amid Inflation Worries

Although it was the last G-10 central bank to switch to a less restrictive setting in September (excluding the BoJ), the Federal Reserve did so emphatically, with an outsized 0.5% cut [4]. With inflation moderating at the time, officials believed it was appropriate to shift their focus to the other part of their mandate and prevent unemployment from further cooling. That choice also illustrated the Fed’s resolve to achieve a soft landing and fend off criticism that it was falling behind the curve.

However, that shift proved premature as the labor market remains robust despite some softness, the economy is doing great, and the disinflation process has stalled. Unemployment is relatively low and far from recessionary, while GDP expanded at a solid 3.1% in Q3. Most importantly, the Fed’s preferred inflation gauge – the PCE – remains well above the 2% target for almost four years. Meanwhile, President Trump’s agenda could further stoke price pressures.

The Fed has turned cautious as a result, with inflation returning as the primary concern. After delivering 100 basis points of easing in just four months, officials now see only 50 bps of cuts in 2025, according [5] to December’s Summary of Economic Projections (SEP). Moreover, they raised the expected longer-run rate to 3% (from 2.9%), but the terminal rate is likely much higher and much closer to the current 4.25-4.5%.

This shallower easing path can pose challenges for the equity market rally and drive USD strength. Such developments could have significant repercussions for the FX market, since they would pressure other currencies. The Indian Rupee, the Mexican Peso and the Chinese Yuan are particularly vulnerable, as many of them are near or at record lows against the greenback.

European Central Bank: More Cuts Needed to Support the Economy

Although it was the first of the Big-3 to pivot back in June, the ECB began its easing journey at a slow pace. However, things changed in the second half of the year as worries around the economy emerged and inflation remained close to the 2% target. With three consecutive moves, the total amount of cuts rose to 100 bps this year, matching the US Federal Reserve.

Still, the European Central Bank remains behind bolder peers like the SNB and the RBNZ and has more work to do on the easing front. Policymakers have a long road to neutral – the level that neither stimulates nor restricts growth - and may actually have to go below that, given the continent’s economic adversities. Euro Area GDP hovers marginally above 0% for the past several quarters.

Officials expect [6] GDP to pick up next year and expand by 1.1% (from 0.7% in 2024), but that seems optimistic. Protracted legislative uncertainty in Europe’s political and economic powerhouses - France and Germany - imperils the bloc’s already frail economy. Additionally, Trump’s tariff threats will aggravate the challenges, as the United States is the bloc’s largest trading partner.

President Lagarde alluded [7] to the unpredictability arising from these situations after the December rate cut, saying “if there is one thing that we discussed in the last two days, it's the level of uncertainty that we are facing”. With coherent fiscal stimulus elusive, the ECB will have to do the heavy lifting on the monetary side and provide forceful easing, with another 100 bps of cuts next year looking reasonable.

Given this difficult backdrop, the ECB sends some dovish signals but refuses to commit to a specific easing path. Data-dependency and meeting-by-meeting decisions remain key tenets of its strategy, fostering ambiguity.

Monetary policy dynamics could continue to weigh on the Euro next year, particularly against the US Dollar. The Fed’s reticence and the need for more easing by the ECB, put EUR/USD at risk of parity. European stock markets can benefit from the easy monetary stance, but economic challenges can pose hurdles.

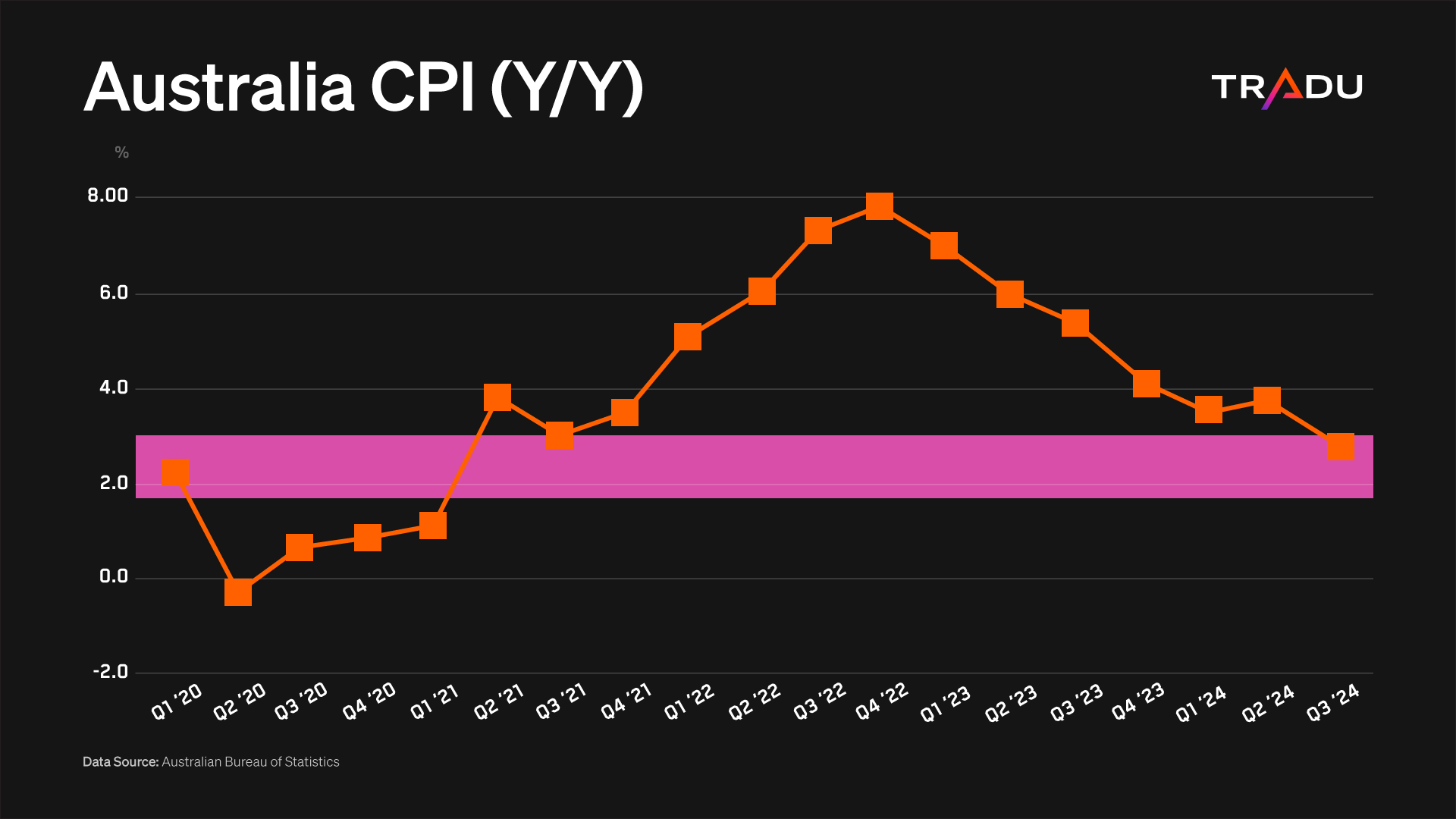

Reserve Bank of Australia: Getting Closer to a Pivot

The Australian central bank is among the notable holdouts in the shift to lower interest rates, keeping them at 4.35% and thirteen-year highs for the past nine meetings. The situation is beginning to change however, as the economy idles and inflation moderated to the lowest levels in almost four years in Q3 and into the 2-3% target range.

Amid these developments, the RBA lays the groundwork for an eventual pivot. In its latest policy statement [8], the Board indicated it is “gaining some confidence” that inflation will sustainably return to the 2-3% target. In addition, officials removed their previous language emphasizing “vigilant” stance and optionality by “not ruling anything in or out”, shutting the door to possibility of rate hikes.

Markets seem optimistic that a pivot can be delivered in one of the first two meetings of 2025, but the road is far from certain. Despite the dovish tweaks in the statement, the RBA has yet to offer clear signals of an imminent shift and there is still good reason for caution. Inflation is elevated, wage growth is still high, and the labor market remains tight.

The late entry to easing from the RBA, as major counterparts may become less aggressive, could put the already weak Australian Dollar at a disadvantage. The currency sheds more than 8% against the greenback this year, reaching nearly five-year lows and the monetary policy differential can exacerbate the struggles.

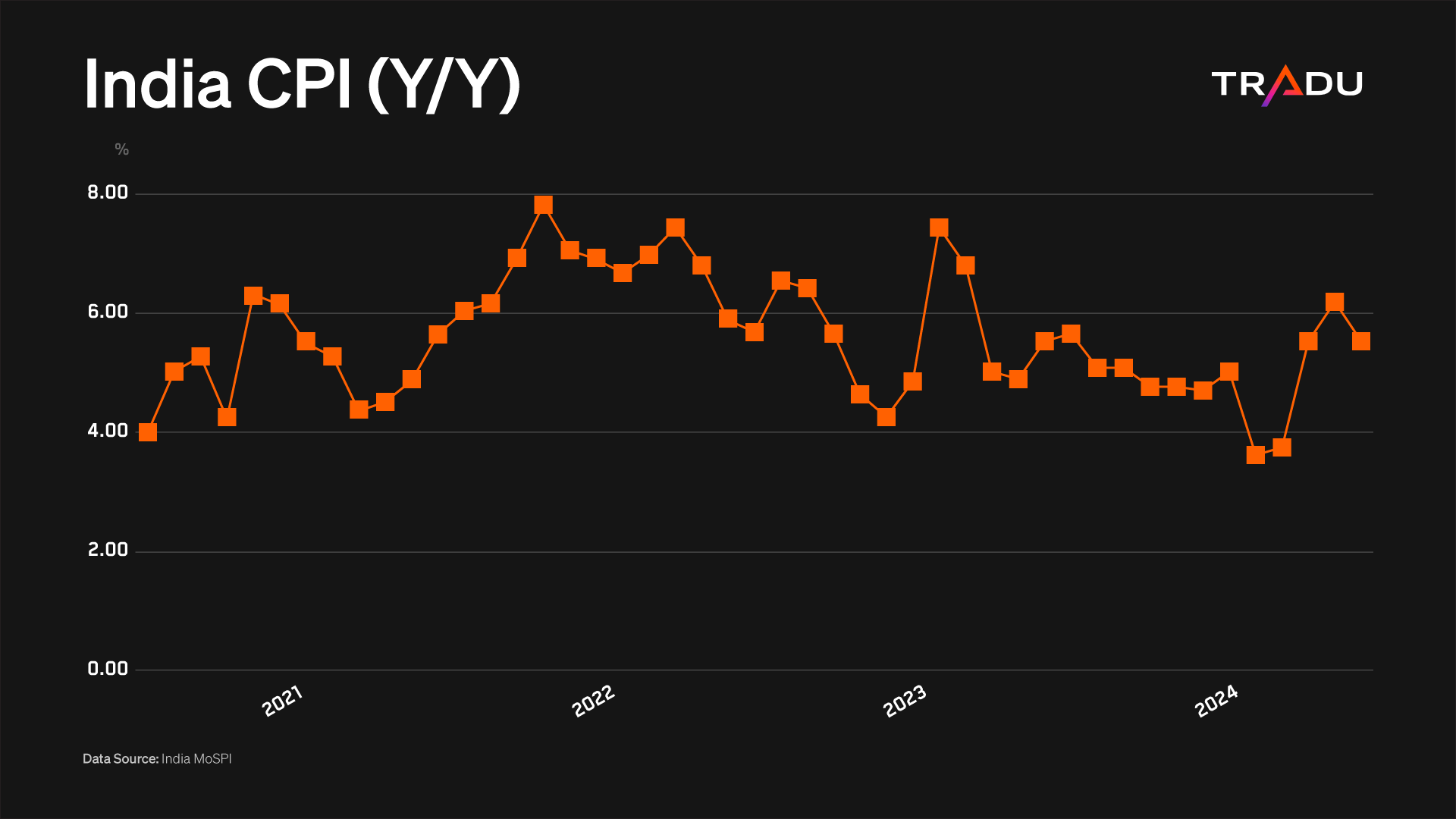

Reserve Bank of India: Gearing Up to Join the Global Easing Trend

At its last meeting in December, the central bank of India maintained [9]rates at 6.5% and their six-year highs, resisting the broader push towards looser monetary policies. Policymakers were guided by a still solid economic expansion and an acceleration in price pressures that caused cracks in the disinflation narrative.

The RBI has stayed on the sidelines for almost two years, under the now former-Governor Das. He is viewed as a hawk and had dismissed concerns that the central bank is behind the curve. But there is a new captain at the helm now, who can facilitate a pivot towards a less restrictive stance. The wheels had already been set in motion earlier this year, when officials shifted [10] to a neutral stance, while inflation eased in November, reinvigorating the disinflation conviction.

Furthermore, India may be the fastest growing major economy, but its momentum wanes: it grew by 5.4% y/y in the third quarter and the slowest pace in two years. Looking ahead, the International Monetary Fund (IMF) expects a slowdown in 2024 and 2025, while prospects of Trump tariffs can aggravate headwinds, strengthening the case for lower rates.

As the RBI readies for such action in 2025, its US counterpart points to cautious easing, creating unfavorable policy dynamics for the Rupee. USD/INR surges 2% this year, repeatedly hitting record highs and a looser monetary stance could continue to provide upward pressure.

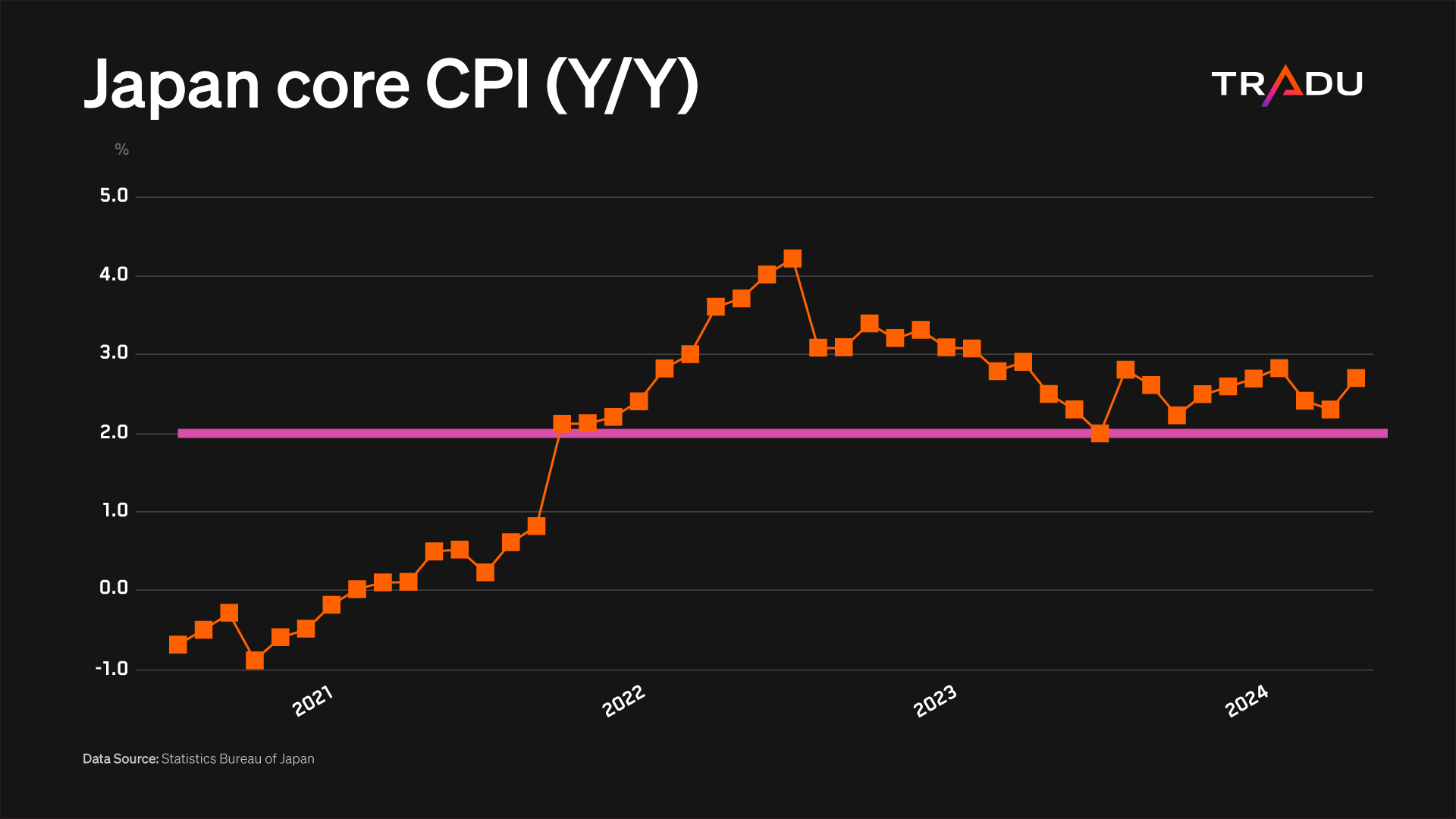

Bank of Japan: More Tightening in Store, but Not a Fait Accompli

While most of its major counterparts started removing monetary restraint this year, the BoJ began tightening, thus staying in the opposite lane. Officials ended the negative rates era in March with the first rate hike since 2007, in a watershed decision [11], driven by persistent inflation, substantial wage increases and Yen devaluation. This was followed by another move in late-July, bringing the cumulative amount of tightening to 50 basis points.

That last increase, however, caught markets off guard and sparked turmoil, sending the Nikkei to an intense three-day plunge. This development led the Deputy Governor to pledge [12] that interest rates would not be raised "when financial and capital markets are unstable" and policymakers stood pat on rates for the rest of the year. Following Japan’s elections, the political landscape does not favor rate cuts either, while looming prospects of trade wars present another deterrent.

Nevertheless, more rate hikes appear likely in 2025, potentially as early as January. Crucially, core inflation has not dropped below the the 2% target for thirty-two straight months and the central bank believes that a virtuous wage-price cycle “gradually intensifies”. At the same time, financial conditions are still accommodative, leaving room for more hikes, while renewed Yen weakness strengthens the case for such action. Still, the extent and pace of future increases remains highly uncertain and the BoJ does not have the best track-record in communicating its intensions.

The Japanese Yen has weakened due to the rate differential with its major peers, especially the US Dollar. This devaluation has repeatedly prompted Japanese authorities to intervene in the FX market to support it. The US Fed projects limited cuts next year and the BoJ is on a cautious and uncertain tightening path. This suggests the Yen's depreciation could continue. On the other hand, the US central bank is still set for further easing and its Japanese counterpart for additional hikes, which would narrow the rate gap and could assist the Yen. Further rate increases by the BoJ may prevent the stock market from fresh highs, but the bullishness has structural drivers that can allow it to maintain its strength.

Uncertain 2025: Setting the Stage for Market Volatility

Global central banks implement looser polices, with notable holdouts likely to join the fray next year. Nevertheless, that does not mean greater alignment, as major institutions are expected to continue operating at different wavelengths. Those that lagged in 2024 could speed up their efforts next year and current frontrunners may become less aggressive. Meanwhile, the Bank of Japan remains an outlier, pursuing monetary tightening. In addition, most major institutions remain non-committal against uncertain macros, amplifying monetary ambivalence.

The diverging paths of central banks have direct implications for both FX and equity markets, potentially fueling volatility. Wall Street appears well-positioned to extend its rally, but a shallower easing trajectory from the Federal Reserve could pose challenges. A stronger U.S. Dollar, in turn, may pressure currencies tied to central banks that adopt more aggressive rate cuts than the Fed, such as the Euro. The Japanese Yen, which remains under pressure against the Dollar, could benefit from a narrowing rate differential.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.