Favorable Backdrop

This has been a strong year for the streaming industry, with Netflix (NFLX.us) reasserting its dominance and legacy entertainment giants finally finding their footing. After making strategic changes, the industry leader was able to accelerate revenue and subscriber growth. Traditional media companies, with the exception of Comcast (CMCSA.us), managed to reach profitability in their DTC segments – a long elusive goal.

Furthermore, Disney (DIS.us), Warner Bros. Discovery (WBD.us), Paramount (PARA.us) and Comcast with Peacock all increased their user bases to new records. Tech giants like Amazon (AMZN.us) and Apple (AAPL.us) that have thrown their hat in the arena don’t report exact figures, but are clearly making strides. Earlier this year, Amazon’s CEO said [1] the Prime video offering had over 200 million monthly viewers. Apple is not as forthcoming, but its Services segment that includes AppleTV+ keeps hitting record revenues.

Subscriber figures will become less important next year though, with Netflix set to stop reporting them, as the industry shifts towards financials and engagement. Advertising inclusive plans are going to be front and center in this shift, while live sports are poised to become even more crucial. The rising proliferation of free streaming options will continue to be monitored, while the Netflix/Disney rivalry will persist.

Shift to Advertising

Netflix abandoned its longtime resistance and offered subscription plans with the inclusion of commercials two years ago, marking a turning point for the broader market. Ad-supported plans are the future for the industry, since they are beneficial to all participants. They provide a lower entry point to consumers, against a difficult economic backdrop that makes them more cost-sensitive and content fragmentation that often leads to multiple subscriptions. Advertisers are also keen to capitalize on streaming. Cord cutting trends make spending on traditional TV less appealing, while this new medium also equips them with more ways to interact with viewers. Most crucially, it offers a new revenue source for streamers that allows them to look past subscription growth as the market matures. There may still be room for growth globally, with Precedence Research expecting [2] compound annual growth rate (CAGR) of 20.9% by 2034, but Europe and North America are getting saturated.

Underscoring the significance and prospects of advertising in the online media landscape, PwC forecasts [3] connected TV (CTV) ads to double from $20.5 billion last year, to $41.2 billion in 2028. That will account for around 28% of global streaming revenues by that time, compared to 20% in 2023. Grand View research expects [4] the global AVOD (Advertising-based Video On Demand) will expand at a CAGR of 29.2% from next year until 2030.

The latest update [5] from Netflix is revealing of the offering’s momentum and potential. It has reached 70 million monthly active users in its ad-inclusive tiers within two years, which now make up more than 50% of new sign-ups in the supported regions. A few weeks earlier, the streaming giant had said [6] it is on track to reach “critical ad subscriber scale for advertisers” in 2025 and was “pleased” with the engagement. Arch rival Disney is also making substantial progress, deliberately pointing customers towards the plans with commercials. In the last quarterly report, executives revealed [7] that “more than half” of new Disney+ subscribers opt for ad-supported tiers. Adding more color, CEO Bob Iger said these plans account for 30% of total DTC subscribers globally. Amazon followed suit this year, introducing advertisements in its Prime Video service. CEO Andy Jassy talked of a “very strong showing” at this season’s advertising upfronts during the last earnings call [8].

The Rise of Live Sports

This move towards advertising-inclusive subscriptions extrapolates the importance of live sports for the streaming market. Such events are naturally suited for ad-placement given half-times and other breaks, while having the ability to draw large and committed audiences on a recurring basis. Sports consistently manage to support traditional TV, resisting the broader shift away from linear networks. The October report [9] from Nielsen, found that NFL, baseball and other competitions helped lift broadcast and cable viewership in October in the US. Still offering limited sports options compared to linear TV, streaming was flat.

The media landscape is evolving rapidly, with streamers increasing their live sports programming, a shift that is already yielding results. The 2024 Paris Olympics were available in the US on Comcast’s Peacock (along with NBC), with Antenna observing [10] 2.8 million sign-ups within a span of seven days. Earlier this year, Paramount aired the Super Bowl LVIII on its streaming platform as well, leading to 3.4 million registrations. And Amazon is solidifying its position as a key player, by hosting NFL Thursday Night Football and securing an 11-year media rights agreement with the NBA, becoming the third partner behind Disney and Comcast’s NBC, in a watershed moment. Apple is also betting on the power of sporting events, hosting baseball (MLB) and soccer (MLS) games.

After spending a long time contained in sports-adjacent programming, Netflix is now venturing into live matches. November’s Jake Paul vs. Mike Tyson boxing match was watched by 60 million households, with most of them tuning in live. Furthermore, the streaming leader will host [12] the WWE Raw tournament from next year onwards. It does not stop there though, in another landmark moment for the industry and the league, it will air two NFL games on Christmas Day. Netflix is pulling out all the stops to draw broader audiences beyond dedicated fans, with mega star Beyoncé set to perform [13] at half-time during the second match.

However, the king of the industry is non-other than Disney, which expected to have spent [14] nearly half of its $25 billion content budget on sport rights in the last fiscal year. It hosts a wide range of competitions across various channels, with ESPN at the forefront, and was able to renew [15] its NBA license through 2036. Now, Iconic CEO Bob Iger is pushing on transitioning ESPN to streaming, with the standalone platform expected in autumn of 2025. This shift could revolutionize the way fans view sports and engage during games.

FAST Growth

The transition away from broadcast TV and towards online video is undeniable, but video on demand-platforms like Netflix are not the only alternative. Content fragmentation, elevated prices and other factors make consumers seek substitutes, which leads them to FAST services.

This stands for Free Ad-supported Streaming TV, which is like traditional linear TV with preset programming and commercials, but online. Such platforms are seeing rapid growth in recent years, with Horowitz Research finding [16] that 66% of US viewers are using them every month, largely due to the appeal of casual channel surfing. Kantar reported [17] a 3% growth in the US in Q3, equal to the increase of paid on-demand ad-supported plans, showing their potential. Some of the most popular FAST platforms like Roku and FOX-owned Tubi are regularly among Nielsen’s ten most viewed streaming channels. In the last report [18] for October, each captured 1.8% share, beating Comcast’s Peacock and Warner’s Max.

It is interesting to see how these platforms will perform next year, but also whether streaming giants like Netflix might be tempted to offer FAST versions. With a cautious entry to live sports and still limited footprint in the broader media landscape, this could be the next logical step for the streaming leader [19]. Such offering would allow it to keep growing its user base and strengthen its advertising position. On the other hand, the advertising value of FAST services is lower than on-demand video, given the more relaxed viewing habits they cater to.

The Netflix vs Disney Showdown

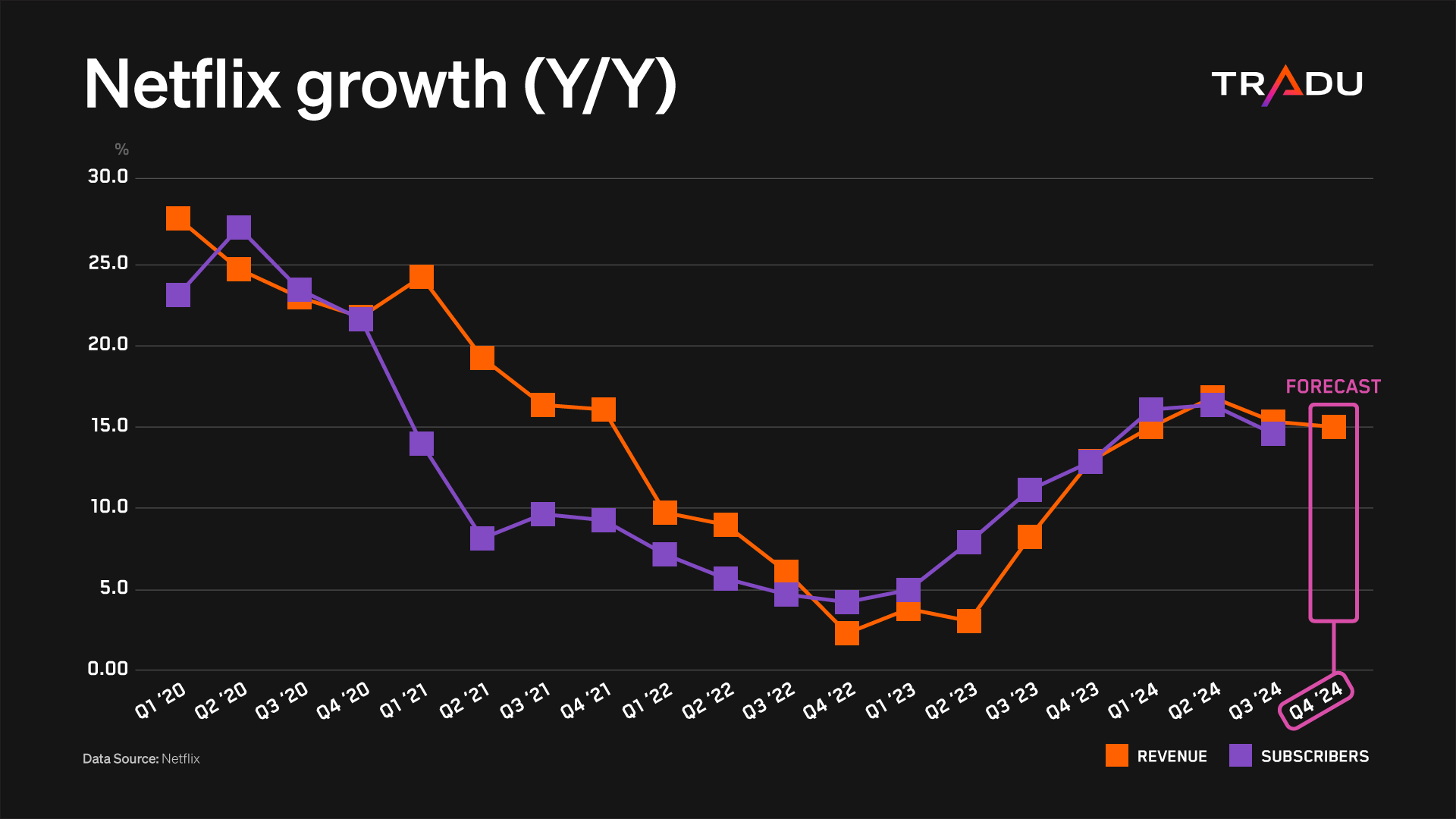

After a shocking loss of subscribers in the first half of 2022, Netflix was forced to rethink key aspects of its business and made two highly successful strategic changes. It cracked down on password sharing, converting shared users into paying members, and introduced lower-priced tiers with the inclusion of advertisements. Both initiatives have worked out beautifully, driving growth in both revenue and subscriber numbers.

Netflix is well positioned for a strong 2025, but next year’s outlook appears more complex. The growth runway from the password sharing change is getting shorter, with revenue and subs heading towards a deceleration for second straight quarter.

Progress on the advertising front is crucial, but despite advancements, it faces a difficult environment. For all its streaming dominance, Netflix remains a relatively small player in the broader media industry and competing with legacy entertainment behemoths is not going to be easy. Nielsen’s media distributor gauge shows [20] that Netflix struggles to make it to the Top-5 of TV viewership in the US. The first place is usually occupied by Disney with its vast network and content portfolio. Engagement is particularly important in this new ad-inclusive era and there are some worrying signs on that front. The company’s latest report [21] revealed that viewership was largely flat in the first half of 2024, compared to the same period a year ago.

The entry into sports can help with that, but the streaming leader has opted for a piecemeal approach. It airs select matches instead of entire leagues and focuses on the drama of the sport to draw in broader audiences. There is good reason for this reserved stance, since securing sports rights is costly and complicated. It is also a technically difficult endeavor and that was evident in Netflix’s October live boxing match which faced various glitches. But Netflix may eventually have to go all in on sports to fend off competition and maintain its leadership.

Netflix’s vast content library remains a key strength, making it a compelling and hard to cancel option. However, in terms of quality it seems to trail competitors. This year it only secured one Oscar [22], with Comcast’s Universal Pictures dominating thanks to Christopher Nolan's Oppenheimer. Although it performed better at the Emmys [23], it could not challenge Disney.

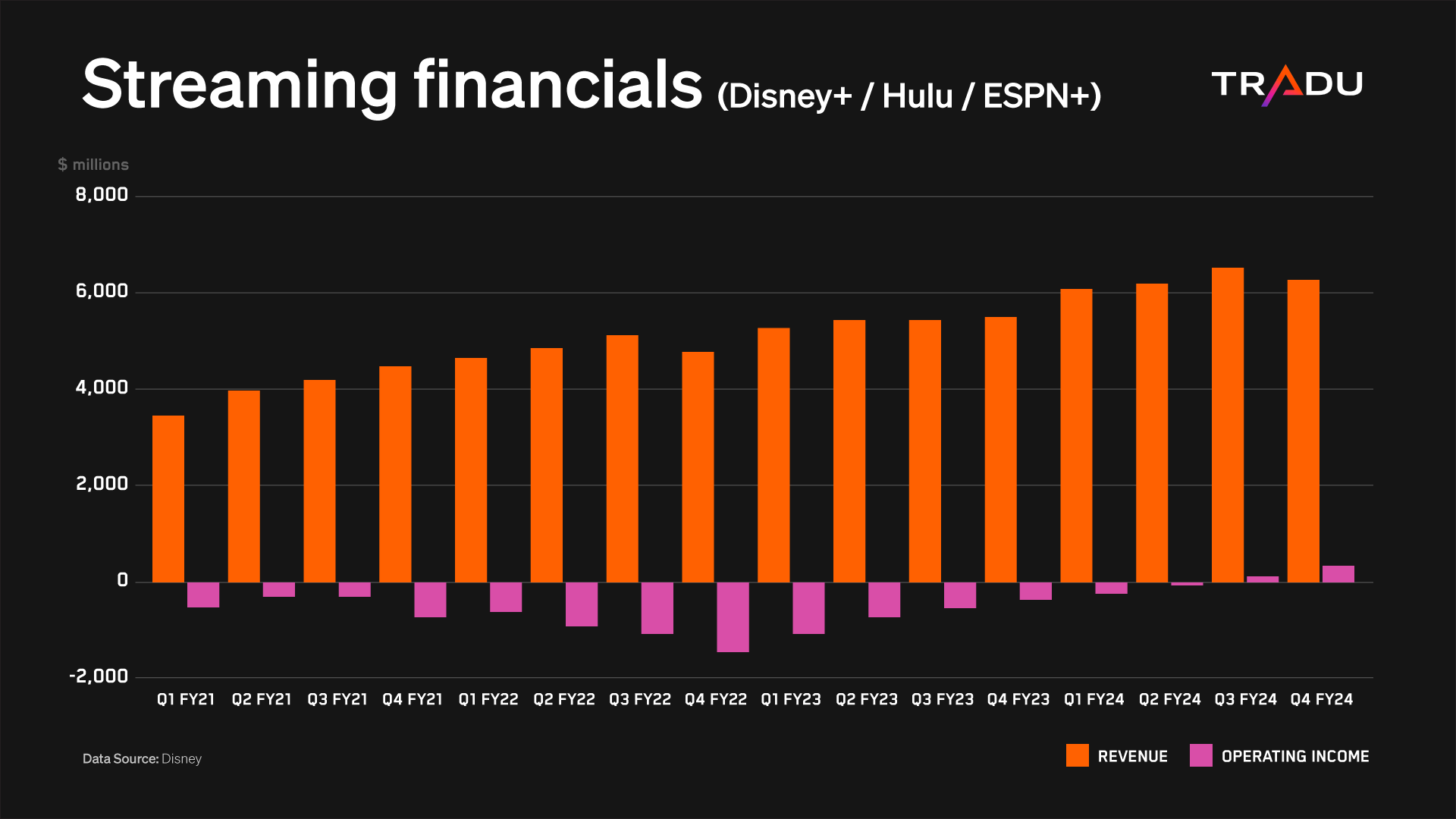

The Walt Disney Company is also primed for a successful 2025, leaving behind the recent adversities, thanks to the CEO’s turnaround strategy. Most notably the company has regained its creative mojo. After the 2023 disappointment and the MCU fatigue, it rules this year’s box office [24] and has a promising 2025 slate. Inside Out 2 and Deadpool & Wolverine occupy the top two spots globally and Moana 2 is climbing fast after its blockbuster Thanksgiving debut. It also shined at the Oscars with five statuettes, led by Poor Things, and swept the Emmys with Shogun and The Bear.

Its streaming subscriber base has returned to growth thanks to the creative resurgence and the success of its ad-supported plans. It has also embarked on its own effort to restrict password sharing and if it performs even half as well as Netflix’s similar effort, Disney could see substantial subscriber growth for several quarters. All of these of course translate into improving financials for its direct-to-consumer business. Crucially, it managed to turn profitable ahead of schedule and executive guidance [25] suggests that operating income could hit $1 billion next year. The broader financials have also been strong and the management expects solid earnings growth in FY25. Disney also boosted [26] its dividend by 33% for 2025, after reinstating payments earlier this year, in a move that will please investors.

Its sport programming is going to play an increasingly important role next year. The launch of the joint digital venture with Warner Bros. Discovery and Fox has bumped onto regulatory hurdles, but Disney moves ahead with its plan to turn ESPN into a streaming platform within 2025. Although not without risks, this shift can unlock tremendous value for the company and take its sport dominance into a whole new level.

Positioned for Success

After a strong 2024, the video streaming industry is well-positioned for success next year. The shift towards advertising is a major catalyst, boosting the top and bottom lines of streamers, while live sports will command an even greater role in driving engagement. Netflix remains the king of the industry and its throne appears secure, but Disney could reemerge as a formidable contender.

However, challenges persist. Intense competition, content fragmentation and persistent signs of financially stressed consumers create potential pitfalls. Netflix’s growth is slowing and Disney’s success is not guaranteed. Meanwhile, other legacy giants like Warner may be hitting their stride in the DTC segments, but they remain in a precarious position and struggles in their linear TV assets continue to weigh on their overall business.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.