Electricity companies surge in 2024

Riding on AI euphoria, Wall Street is up by around 25% in 2024, enjoying consecutive record highs. The US economy has remained strong, and interest rates have been coming down. The Trump-effect has further boosted the prevailing bullishness. The rally is largely concentrated around Big Tech, but the surge spills over to other sectors, bringing a usually overlooked segment into the spotlight – utility companies.

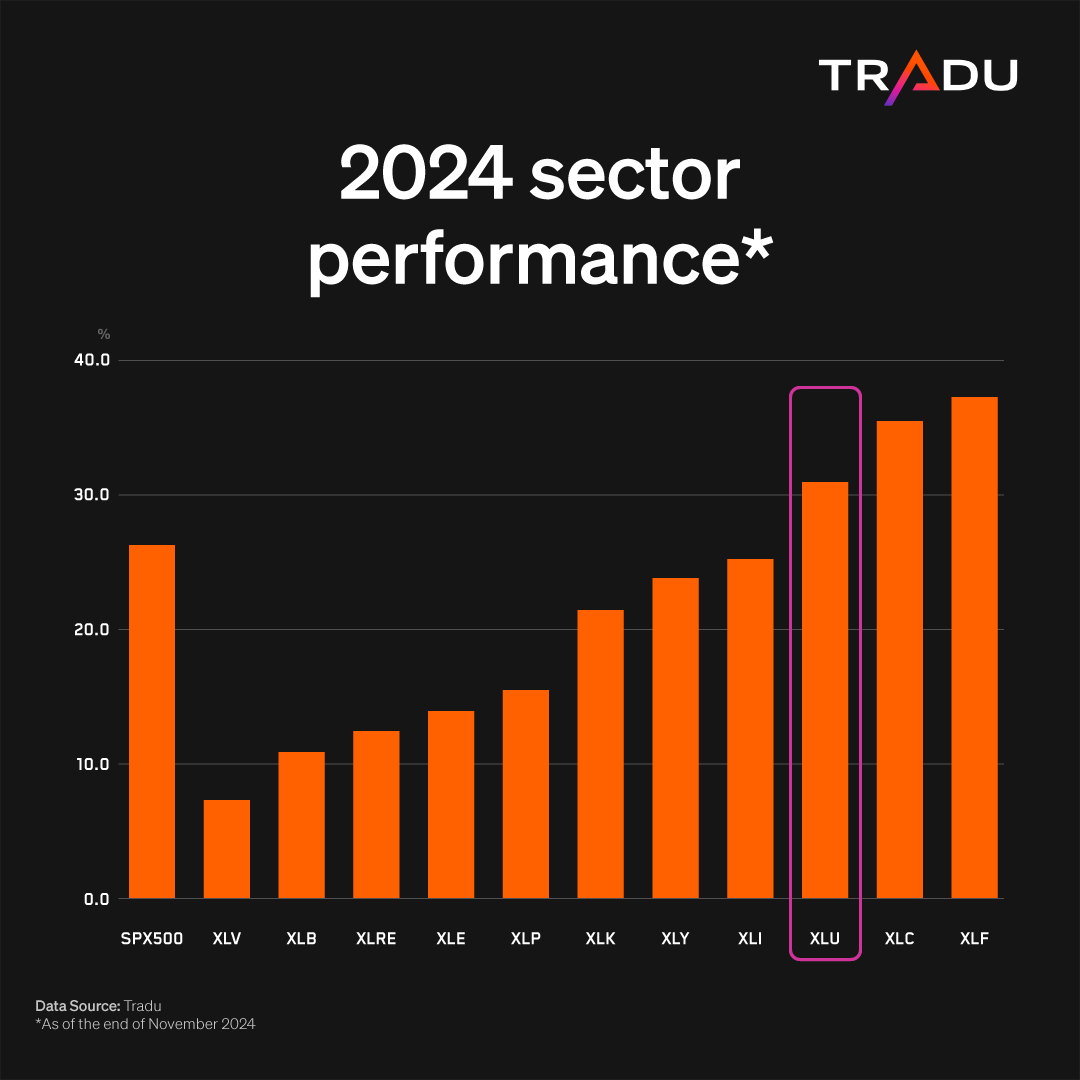

Such corporations rarely spark excitement, especially during periods of exuberance like the current one. The sector is a classic defensive play, benefiting mostly when things are not going well, as investors seek stable performances and dividends. But the situation has been different this year since the sector is among the best performers of the S&P 500, with the Utilities SPDR ETF (XLU) rallying over 30%.

Following years of stagnation electricity demand has been rising, and there appears to be room for further expansion. Broader electrification, reshoring of American manufacturing, extreme weather conditions and a growing population are among the drivers. But there’s now a new factor in play – AI.

AI and EVs take off together

The proliferation of AI and electric vehicles will continue to play a paramount role in 2025, and shape the fortunes of the industry. The Trump Presidency is going to be another catalyst, offering both opportunities and reasons for caution, while key players like Vistra will be closely monitored.

Big Tech companies vie for AI market share

OpenAI’s ChatGPT kick-started the Artificial Intelligence boom two years ago, in a technological leap that rapidly filters through every aspect of daily life and could shape the future of humanity. Tech giants are locked in a battle for AI supremacy, spending heavily to develop their capabilities in the field.

Microsoft appears to be at the forefront of this revolution, thanks to its massive investments in OpenAI, weaving AI features into a broad range of products for retail consumers and enterprises. Alphabet was initially caught off guard, but has been moving swiftly to catch up. Meta is another pioneer, spending more and more to advance the technology that drives engagement on its platforms and increases advertising revenue. Apple made a belated entry this year. Its rival, Samsung, has been pushing on the front for longer. Their combined involvement is likely to further accelerate the proliferation of AI.

Data centres grow to feed AI

With its infrastructure being the go-to solution for training and inference of large language models, Nvidia is the enabler and main beneficiary of the boom. Data Center sales have surged 170% y/y in the nine-month period through October. Nvidia is accelerating its AI cadence, and the latest Blackwell architecture is in full production, according to the CFO’s comments on the last earnings call [1]. Ms. Kress also said that shipments will ramp up next year and anticipates Blackwell to generate several billions of revenue in the current quarter.

This transformative technology provides another demand accelerator for data centres. McKinsey & Company expects [2] global demand for data centres to more than triple by 2030, with 70% of that demand coming from facilities that are able to host advanced AI-workloads.

The development and deployment of AI models requires vast amounts of computing power and energy, with the data centre expansion further dialing up electricity usage. In its latest outlook [3] (STEO), the US Energy Information Administration (EIA) forecasts an increase of around 1.9% y/y this year and the next, reaching new-record levels. In a recent commercial consumption report [4], the organisation found that the 2023 growth was “concentrated in a handful of states experiencing rapid development of large-scale computing facilities”.

AI consumes heavy amounts of electricity

Underscoring the energy-intensive nature of AI, the International Energy Agency (IEA) found [5] that a ChatGPT query requires 2.9 watt hours (Wh) of electricity compared to just 0.3 Wh for a typical Google search - an eye-watering jump of 867%. More than 30% of the world’s server farms are located in the US and the IEA projects their electricity consumption will shoot up from 200 TWh in 2022 to almost 260 TWh in 2026.

Big Tech is making moves to ensure adequate electricity supply for their energy-hungry AI models, focusing on carbon-free resources, with nuclear power gaining traction. Microsoft announced an agreement [6] with Constellation Energy to restart a unit of the Three Mile Island nuclear plant and add approximately 835 megawatts (MW) of carbon-free energy to the grid. Google has inked a deal [7] with nuclear energy firm Kairos, totaling 500 MW by 2035. Amazon has followed suit with its own nuclear agreements [8]. Nuclear energy enjoys bipartisan support and the Biden Administration has set out a plan [9] to triple capacity by 2050.

EV proliferation dials up demand for electricity

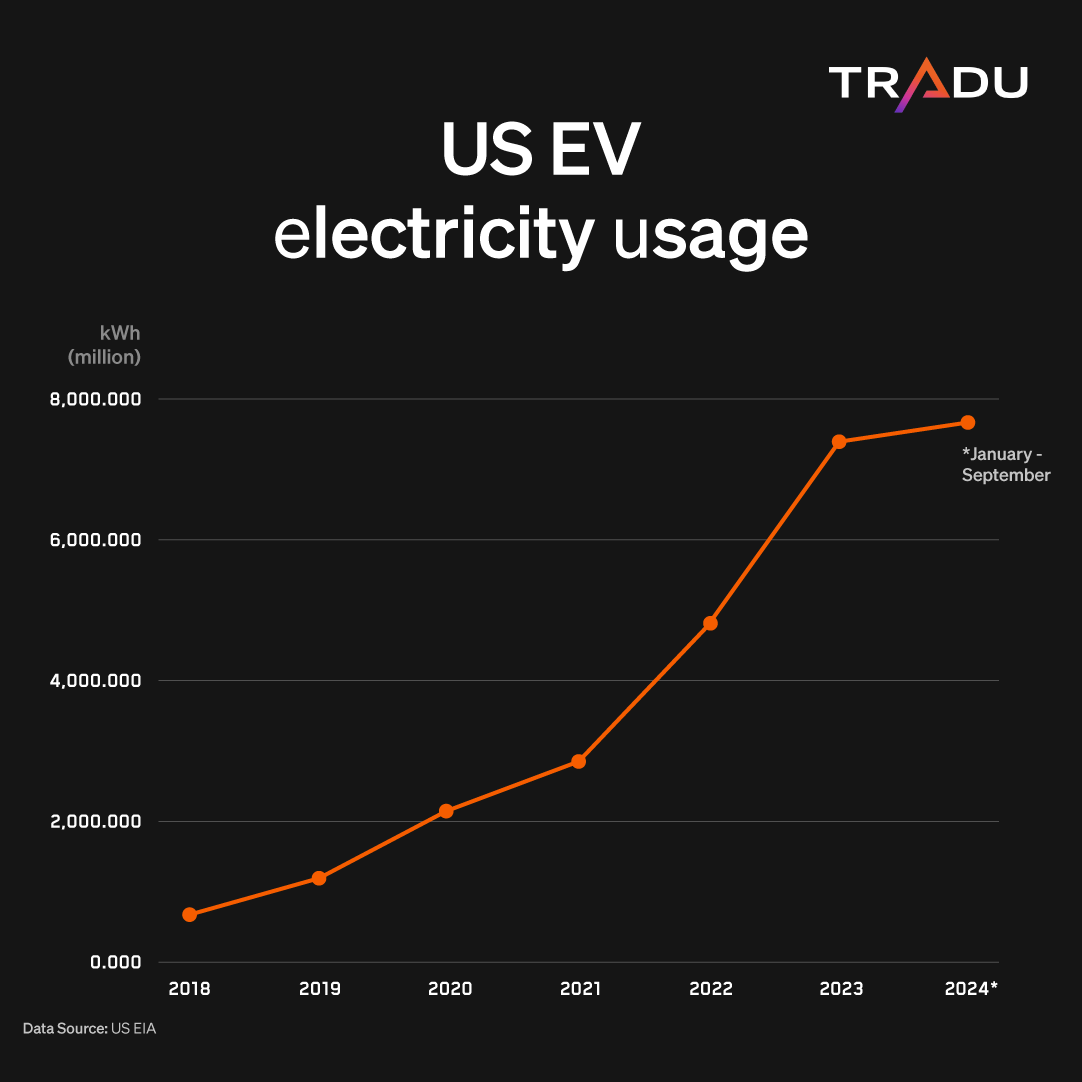

The shift away from fossil fuels is another crucial piece of the power consumption puzzle, as the automotive industry shifts towards electric power to facilitate this transition and meet emissions targets. J.D Power expects [10] 1.2 million sales this year in the US, and a market share of 9%, while forecasting a rise to 36% by 2030. In an important milestone, the bestselling car of 2023 was Tesla’s Model Y, according [11] to Jato Dynamics. Despite challenges, the charging network also keeps expanding, with more than 200,000 ports [12] around the country (Level2 & Fast DC). Tesla has installed 750,000 Powerwalls worldwide based on a recent update [13]. The adoption of e-mobility leads to increased electricity consumption, which is already at record levels this year.

The appeal of EVs may have diminished over the last couple of years against unfavorable macros and high prices, but the setback seems temporary, and their proliferation unstoppable. The current administration has established a series of incentives and massive spending packages to facilitate the industry’s growth. More affordable vehicles and autonomy can propel the industry forward and continue to drive up electricity usage. Tesla, and other manufacturers like General Motors, plan lower-priced models for 2025. Musk is also investing heavily in fully self-driving vehicles, again powered by electricity.

An ageing grid and AI uncertainty lie ahead

Not everything is coming up roses though, as the sector faces a series of potential pitfalls. Top among them are concerns over the antiquated state of the US electricity grid, which may struggle to cope with the generational growth in demand. Berkeley Lab found [14] that the backlog of new power generation and energy storage seeking transmission connections across the US grew by 30% last year.

That said, AI becomes more efficient as the technology advances, and, as such, power usage could be mitigated. Nvidia’s latest Blackwell [15] platform reduces energy consumption by 25 times compared to its predecessor, for instance, while Amazon has launched [16] tools to make its data centres less power-hungry.

AI’s advance may lose momentum as compared to the previous two years. CEO of Alphabet, Sundar Pichai, hinted [17] at such likelihood, saying, at this year’s New York Times DealBook Summit: “I think the progress is going to get harder. When I look at 2025, the low-hanging fruit is gone.” Additionally, the actual benefits of AI may be exaggerated. Nobel laureate MIT Professor Daron Acemoglu (co-author of the coveted Why Nations Fail) recently estimated [18] only modest benefits to productivity and GDP over the next ten years.

On the clean energy front, demand for electric vehicles in the US is slowing down, and further expansion of the charging network is needed. The country still relies too much on fossil fuels for energy generation. Reliance on natural gas may be a good option for this transitional period, but does not provide a long-term solution.

The Trump-effect on the energy sector as a whole

The electoral victory of President Trump can prove a catalyst for the future of utility companies, but it is unclear whether his policies will boost them or pose hurdles. It may be telling that the XLU ETF has largely been flat since the election, just as other sectors like Financials (XLF) soared.

President Trump ran on a deregulation agenda [19], with fewer restrictions being financially beneficial for the future of this heavily regulated industry. The AI power push makes this more crucial, especially after the rejection [20] of the Amazon-Talen nuclear deal by the Federal Energy Regulatory Commission. A pledge for lower taxes and potential reshoring acceleration from isolationist policies can all have a positive impact.

Trump’s promise to unleash energy production, including nuclear, is pivotal. Less than 20% of electricity usage is covered by this source, but its importance increases as Big Tech turns to it to power AI. However, his stance on the matter appears to be ambivalent. Speaking at the Joe Rogan Experience in October, he took note [21] of the benefits of nuclear energy, but also highlighted the dangers, adding that nuclear plants “get too big and too complex and too expensive”.

Trump has also vowed to undo the clean energy initiatives of the current administration, which could harm the adoption of electric vehicles and constrain energy consumption. Abolishing the $7,500 federal tax credit for EVs, could lead to a 27% drop in registration according to recent research [22] entitled The Effects of “Buy American”: Electric Vehicles and the Inflation Reduction Act.

Furthermore, his polices are likely to have a reflationary impact that could force the Fed to adopt a shallower and slower easing path. Electricity firms generally have high debt levels, so elevated interest rates would create significant financial headwinds.

Dealmakers in the spotlight: Vistra, Constellation & Entergy

Vistra is the main beneficiary of the sector’s increased appeal, with its stock rallying around 280% year-to-date. This makes it the second-best performer of the S&P 500, easily beating Nvidia, and surpassed only by Palantir.

The company operates across many US States, serving more than 5 million customers, with capacity of 41,000 Mega Watts (MW). Most of it comes from natural gas - the bridge fuel that is the go-to source of electricity for companies trying to reduce reliance on fossils. Nuclear is the third largest source. This mix places it in a strong position to capitalize on the expansion of data centres and the shifting trends of the industry. It has announced solar deals with Microsoft and Amazon, but nuclear and gas agreements remain elusive, which could put it behind more active rivals. Executives are working to change that, though, and mentioned discussions with large companies and hyperscalers on both fronts, during the Q3 earnings call [23].

The Texas-based firm topped expectations with its latest results, and runs a strong financial year, with revenues and profits up double digits in the January-September period. More importantly, management admits that adjusted profits (EBITDA) may rise significantly this year and the next.

Although smaller in terms of capacity, with 32,400 MW, Constellation Energy serves 16 million homes and businesses across most US States. Its portfolio is predominantly nuclear, and it has already signed a landmark agreement with tech giant Microsoft, which puts it at the forefront of the race to power generative AI.

Its stock has doubled this year, largely fueled by its AI advances, although regulatory uncertainty poses potential risks. Constellation firmed up its 2024 operating earnings guidance, although, according to a somewhat mixed report [24], revenues are down 4.9% in the nine months to September.

Entergy is another leader in the push to cover the energy needs of AI and data centre expansion. The firm will power [25] Meta’s largest hyperscaler data centre, worth $10 billion, as announced in December. Earlier in the year, Entergy struck a deal [26] to provide electricity to Amazon’s new AWS data centres in Mississippi. Its stock has rallied nearly 50% this year, helped by these initiatives, with a two-for-one stock split performed in December.

The firm operates in four US states, reaching three million customers. It has a capacity of 24,000 megawatts, with most of it coming from natural gas, nuclear being the third generator. Executives are discussing expansion of the latter, according to the Q3 [27] earnings call. However its large coal and oil footprint, along with its small renewables contribution, may put it at a disadvantage.

The company’s revenues are down 3% y/y in the nine months to September, and net income nearly halved, partly due to hurricane-related outages. Management offered an optimistic outlook, though, expecting higher earnings and dividends in the next four years.

Any major headwinds for utilities during 2025?

The breakaway success of the Utilities sector this year sets the stage for another strong performance in 2025, as its key drivers are likely to persist. Added to which, investments in Artificial Intelligence and data centres are set to continue as electricity companies are on a deal-making spree with Big Tech to power their burgeoning energy demands. Vehicle electrification progresses despite setbacks, and may be due a better year ahead. Trump’s return to the White House offers reasons for optimism, especially if he opts for looser regulations.

He could also create a more complex macro environment through higher interest rates, tighter immigration and fossil fuel commitment that can slow the EV proliferation. Additionally, electricity companies need to make significant investments to increase their capacity, while the pace of AI advance could lose some of its momentum.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.