Commodities

Gold market outlook: Can the rally continue in H2 2025?

Risk aversion driven by Trump tariffs, heightened geopolitical tensions, US dollar weakness, and robust central bank buying have been the cornerstones of gold’s rally in 2025. Bullion demand is expected to remain strong in H2 2025 as trade uncertainty lingers, global security risks persist, and de-dollarization trends continue. However, dollar negativity may have peaked, elevated interest rates are not good for non-yielding assets, and Gold’s safe haven appeal could fade sentiment improves.

Key drivers of gold prices in 2025

Gold surges this year, driven by its enduring safe-haven appeal amid a range of developments fuelling risk aversion. Geopolitical uncertainty drives risk-off inflows, underscored by the Israel-Iran conflict that saw the US bombing the latter’s nuclear facilities. Meanwhile, the war in Ukraine drags on, with NATO members ramping up military spending to adapt to an increasingly unstable security landscape.

Trade tensions are also at the top of the list and hardly a day goes by without the topic dominating the agenda. Sweeping tariffs imposed by the US President risk derailing the global economy and fuelling inflationary pressures, creating a fraught macroeconomic backdrop.

Central bank buying has been another bedrock of bullion demand against trade, economic, and geopolitical uncertainty, as well as a broader de-dollarization trend. US Dollar weakness compounds gold’s strength, having emerged as a key casualty of Trump’s policies.

Learn more about how to trade commodities.

Geopolitical tensions drive gold demand

Despite President Trump's stated aim to avoid foreign conflicts and end ongoing wars, his return to the White House has coincided with a surge in geopolitical instability. His repeated claims over territories such as Panama and Greenland [1] raise alarms, while his approach to Ukraine and the continuation of that war have heightened security concerns across Europe.

The most serious episode of his second term has been the Israel–Iran conflict, culminating in US airstrikes on Iran’s nuclear facilities. Although a ceasefire was quickly reached after that, doubts persist about its durability - especially as the status of Iran’s nuclear programme remains unclear. While President Trump insists the facilities have been “completely and totally obliterated” [2], various reports suggest only limited damage [3]. Moreover, the International Atomic Energy Agency is unaware of the current location of Iran’s 400 kg of uranium enriched to 60%. [4]

Highlighting the uncertain geopolitical environment, Europe is making a historic rearmament effort, while Trump’s One Big Beautiful Bill pushes the US security budget past $1 trillion as President Trump pursues his Golden Dome Initiative. Meanwhile, NATO agreed to increase defence spending to 5% of GDP by 2035 [5]. The resulting boom in orders, revenue, and share prices for defence contractors such as Renk, Rheinmetall, and Northrop Grumman reflects this shift.

Trade uncertainty fuels risk-off flows

President Trump’s re-election has been marked by aggressive trade policies that disrupt global supply chains and stoke economic uncertainty. Following sectoral tariffs on autos, steel, and aluminium, he introduced 50% duties on copper imports this month, pushing prices to new record highs. He has also renewed threats of levies on pharmaceuticals and semiconductors. [6]

On April 2, dubbed Liberation Day, the President launched reciprocal tariffs on key trading partners but temporarily lowered them for 90 days after market turmoil. With this grace period having expired, President Trump begun sending out letters informing partners of the tariffs they will face starting August 1, including the European Union, Japan, Mexico, and more. While trade negotiations are ongoing, progress is limited. A truce with Beijing has been agreed that lowers previously prohibitive duties on Chinese imports to 30%, but details are elusive and the rate is still high.

These measures, along with the surrounding uncertainty, risk increasing business costs, eroding margins, dampening investment, raising inflation, weakening consumer demand, and slowing global growth. Reflecting these challenges, the World Bank recently cut its 2025 global growth forecast by 0.4 percentage points, citing “increased trade tension and heightened policy uncertainty”. [7]

World Bank key 2025 GDP forecasts:

- United States: 1.4%, from an estimated 2.8% last year

- Euro Area: 0.9%, from an estimated 0.9% lats year

- China: 4.5%, from and estimated 5% last year

- India: 6.3%, from an estimated 6.5% last year (on fiscal year basis)

US Dollar weakness supports gold’s appeal

The greenback emerged as a key casualty of Trump’s disruptive policies, which erodes confidence and its risk-off appeal. Bullion benefited from these capital shifts and emerged as the safe haven of choice against heightened macroeconomic risks. These dynamics could persist in coming months, as the dollar may continue to face headwinds, while President Trump has a clear track record of talking down the dollar.

The One Big Beautiful Bill has stokes fears over the mounting US debt, with the Congressional Budget Office estimating an increase in deficit of 3.4 trillion over the next nine years. [8] This comes at a period when the negative effects of tariffs are hitting home.

While the Federal Reserve has adopted a cautious stance, citing a strong labour market and persistent inflation, it may be forced to ease policy soon. According to the Fed’s latest projections, officials anticipate a median policy rate of 3.9% by year-end [9] - implying two rate cuts. Such a shift could further weaken the dollar, especially as central banks like the ECB wind down their own easing cycles.

Concerns over the Fed’s independence are also resurfacing. President Trump has repeatedly criticised Chair Jerome Powell for resisting further rate cuts and has again called for his resignation this month, describing such a move as “a great thing” [10]. Meanwhile, NEC Director Kevin Hassett told ABC’s This Week that Powell’s removal is “being looked into” by the administration. [11]

Central bank demand is a linchpin of gold’s strength

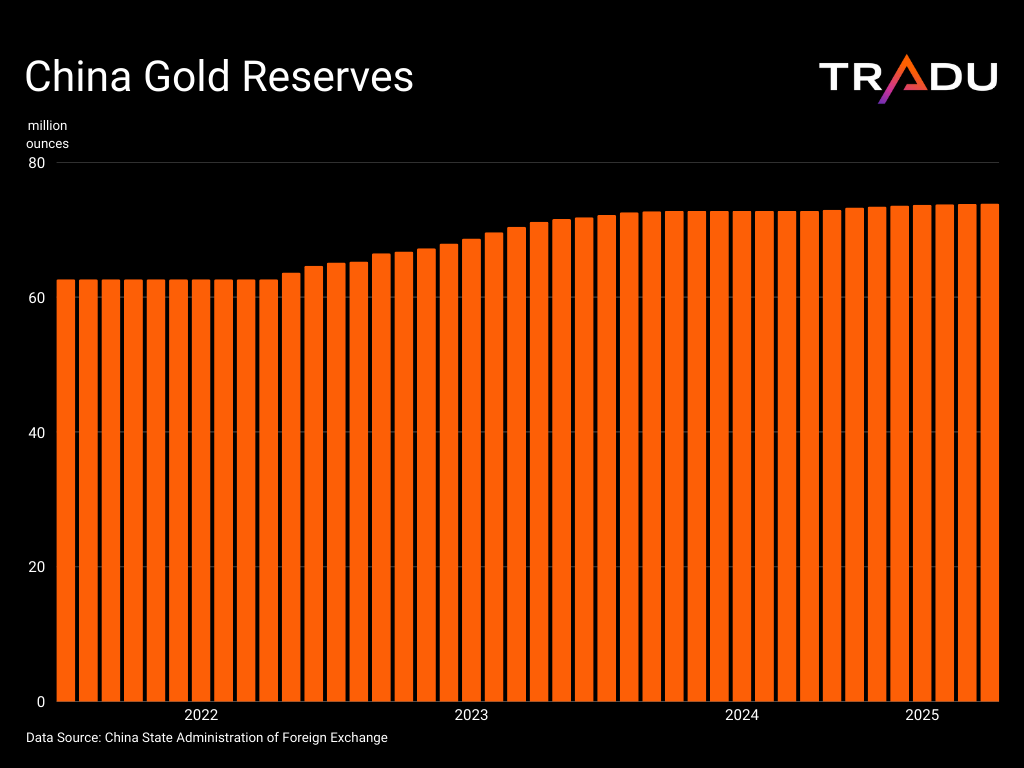

Central bank hoarding has been instrumental in the rally of the precious metal over the last couple of years. Emerging economies are at the forefront of this shift as they try to lower their dependence on the greenback to mitigate currency risks and hedge against inflation. According to an ECB study, central bank buying reached record levels in 2024, accounting for 20% of total global gold demand - making gold the second-largest reserve asset.

China spearheads this shift away from the US Dollar and towards the precious metal, having increased its reserves for an eight straight month in June, despite the record high prices.

Trump tariffs and the related macroeconomic uncertainty plays into these fears, threatening to exacerbate the de-dollarization trend in favor of gold. The 2025 Central Bank Gold Reserves (CBGR) survey by the World Gold Council found that a majority of respondents anticipate “moderate or significantly lower” US dollar holdings over the next five years. Additionally, 43% expect to increase their own gold reserves within the next year, with emerging and developing economies the most inclined to do so. [13]

Can gold maintain its momentum in H2?

Global uncertainty drives trading interest in gold, with volume among clients* almost doubling in the first half compared to the same period last year, in a theme that could continue to resonate in the coming months.

With geopolitical and trade-related risks unresolved, the appetite for safe-haven assets may remain strong. At the same time, central bank buying and USD weakness may linger. Such developments would continue to fuel demand and keep XAU/USD on track for new all-time highs.

Source: www.tradingview.com

On the other hand, the blockbuster performance may be hard to replicate in the latter part of the year. Investor fatigue has emerged following April’s record peak, with the Israel–Iran conflict failing to push prices to new highs. Markets also appear to be growing desensitised to ongoing tariff talk.

Now that much of the US trade agenda has been laid out—and with potential deals on the horizon—tensions may ease, diminishing gold’s defensive appeal. Meanwhile, the US economy has shown resilience in the face of headwinds, and stubbornly high inflation could deter the Fed from easing as aggressively as markets expect. Even if two cuts materialise, interest rates would remain elevated - posing a headwind for non-yielding assets like gold.

Moreover, the dollar is showing signs of recovery, suggesting that peak negativity may be behind us. These dynamics could expose gold to correction. Still, a break below the 200-day EMA (around $3,000) would be needed to challenge the current bullish trend.

*Stratos clients

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.