Shares

Can Nike bounce back? Q4 FY25 Miss, tariff headwinds, and the road to recovery

Nike’s troubles deepened in the latest quarter, as revenues continued to decline. Trump tariffs pose an existential threat due to the brand’s manufacturing footprint in China and across Asia. These challenges compound existing headwinds from strategic missteps and fierce competition from Adidas, On Running, and others. However, Nike is taking the right steps towards recovery, and the outlook for the current quarter suggests the worst may be over—raising hopes for a rebound in the stock.

Strategic missteps are still hurting Nike’s performance

The sports apparel and footwear giant has been going through a rough patch over the past couple of years. At the crux of Nike’s travails is a botched shift in its sales channels. Under previous leadership, the firm prioritised its own sales channels (Nike Direct), even though more sales came through third parties. This misstep is also evident in foot traffic data, with visits to Nike stores trending negatively for the past eight months, according to Placer.ai [1]. Although the strategy made sense during the pandemic, it ultimately proved costly - hurting relations with retail partners and diminishing brand visibility.

Another significant issue was Nike’s overreliance on lifestyle products, flooding the market with endless iterations of Dunks, Air Force 1s, and Air Jordan 1s. This oversaturation diminished their appeal, with consumers increasingly turning to rival lifestyle sneakers such as the Adidas Gazelle and Samba. Nike lost part of its core identity by leaning too heavily on these products while falling behind in innovation. These missteps paved the way for legacy rivals like Adidas and innovative upstarts such as On Running and Hoka to chip away at Nike’s market share.

Tariffs threaten Nike’s profitability and demand

Trump-era tariffs compound Nike’s self-inflicted wounds, making the macroeconomic environment even more hostile and hampering recovery efforts. Nike manufactures most of its products in Vietnam, China, and other Asian countries [2]- all now facing steep levies. These actions are expected to squeeze Nike’s profits, with CFO Matthew Friend referring to a “new and meaningful cost headwind” of around $1 billion during Thursday’s earnings call. [3]

Nike can’t avoid passing these costs on to customers. Mr Friend announced a “surgical price increase” in the United States starting this autumn. However, such price hikes risk hurting demand- particularly at a time of weak consumer confidence, ongoing stagflation fears, and persistently high credit card delinquency rates. Discretionary purchases such as plane tickets, smartphones, and sports apparel are the first to be cut by financially strained households during economic downturns, making Nike especially vulnerable in the current climate.

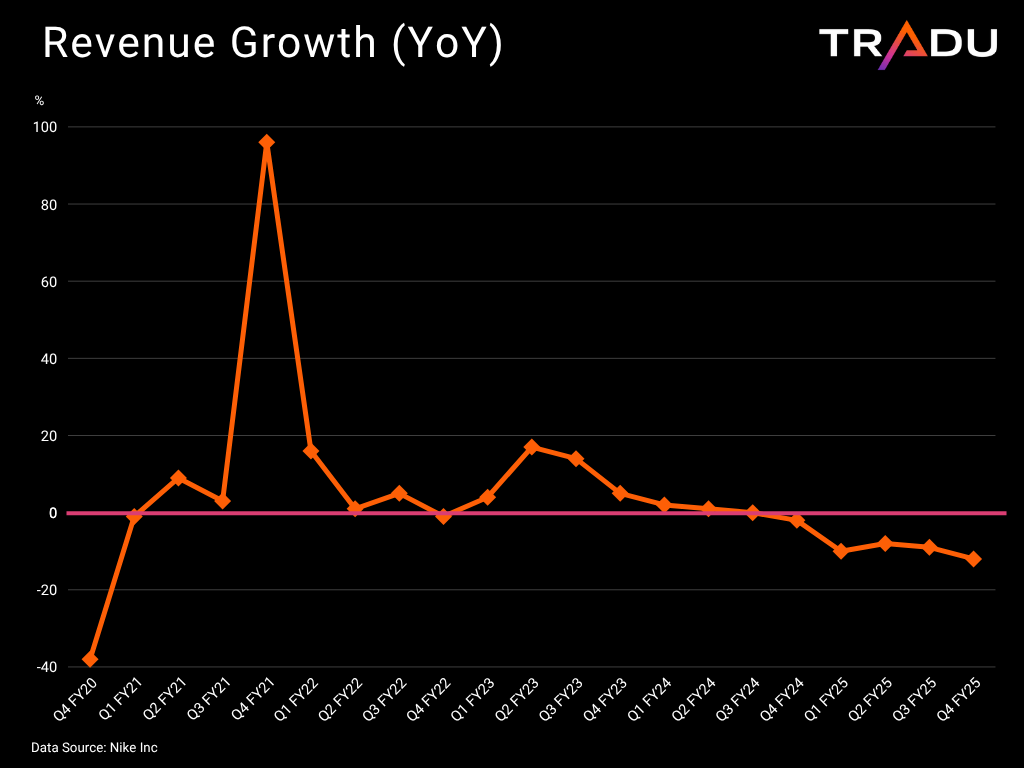

Nike Q4 FY25 revenue falls sharply amid ongoing challenges

Thursday’s results for the quarter ended 31 May (Q4 FY25) underscored Nike’s ongoing struggles, with both revenue and profit falling sharply. During the earnings call, CEO Elliott Hill admitted the results were “not up to the Nike standard”.

Net income came in at just $200 million, dropping by a massive 32% y/y, while gross margin narrowed further to 40.3%. Revenues dropped 12% y/y, to $11.097 billion, marking the steepest decline in five years. Sales across all geographic regions fell, led by a 21% decline in Greater China [4]. With inventory was flat, revenues will continue to face pressure as the company relies on discounts to burn offload older merchandise and make way for new products.

Nike’s turnaround strategy: Is recovery on the horizon?

Despite the grim results, Nike’s guidance suggests a possible bottoming out. CFO Matthew Friend expects headwinds to “moderate from here”, with revenue projected to contract by “mid-single digits” in the current quarter. If so, it would mark the smallest decline in over a year.

Nike is making all the right moves to turn things around, after recognizing its strategic mistakes. The company is repairing its relationship with third-party sellers, with CEO Elliott Hill personally meeting with partners to reaffirm that the brand is now “prioritising and investing in their businesses”. Indicatively, wholesale revenues improved sequentially in the reported quarter, while direct sales continued to decline. Underscoring this shift towards a diversified multi-channel approach, is Nike’s return to Amazon. Wholesale revenues improved sequentially in the reported quarter, while direct sales continued to decline.

Nike is also doubling down on its core sports identity. Its running division grew by “single digits” in Q4 FY25, bucking the broader downward trend. The company is trying to regain its innovation edge with new cushioning technologies, AI-powered designs, 3D-printed sneakers, and more. Meanwhile, NikeSkims aims to increase appeal among female consumers and reclaim market share from brands like Lululemon.

Nike stock outlook

The revenue guidance indicates that Nike’s turnaround efforts may be gaining traction—potentially lifting investor sentiment and supporting a rebound from the multi-year lows reached following Trump’s so-called “Liberation Day”. A move above the 200-day EMA would neutralise the bearish outlook and open the door towards fresh 2025 highs.

However, Nike’s actions will take time to yield results, and Trump’s disruptive trade policies are complicating the recovery. As such, NKE remains vulnerable to renewed pressure and the risk of fresh multi-year lows.

Source: www.tradingview.com

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.