Shares

US Travel industry faces major threat from Trump tariffs

The Trump-era tariffs and resulting economic instability are placing severe strain on the US travel and hospitality industry. With both domestic and international tourism declining, Airbnb, Hilton, Delta Air Lines, United, and other travel firms are being forced to revise financial expectations. Nonetheless, strong fundamentals and potential policy shifts may provide light at the end of the tunnel.

Trump tariffs spark economic headwinds for US travel and hospitality

The US travel and hospitality industry is facing serious challenges due to Trump's tariffs and rising macroeconomic uncertainty. On 2 April, President Trump introduced sweeping trade tariffs on trading partners and long-standing US allies . While some tariffs have been paused, many remain, disrupting global trade and threatening a significant economic slowdown - with direct consequences for travel demand.

The International Monetary Fund warned of “a major negative shock to growth” as it revised its forecasts downward. It now projects global GDP growth of 2.8% for this year (down from the previously expected 3.3%) and has cut its US GDP forecast by 0.9 percentage points to 1.8% . Preliminary data show the US economy shrunk by 0.3% in Q1 - the first contraction in three years.

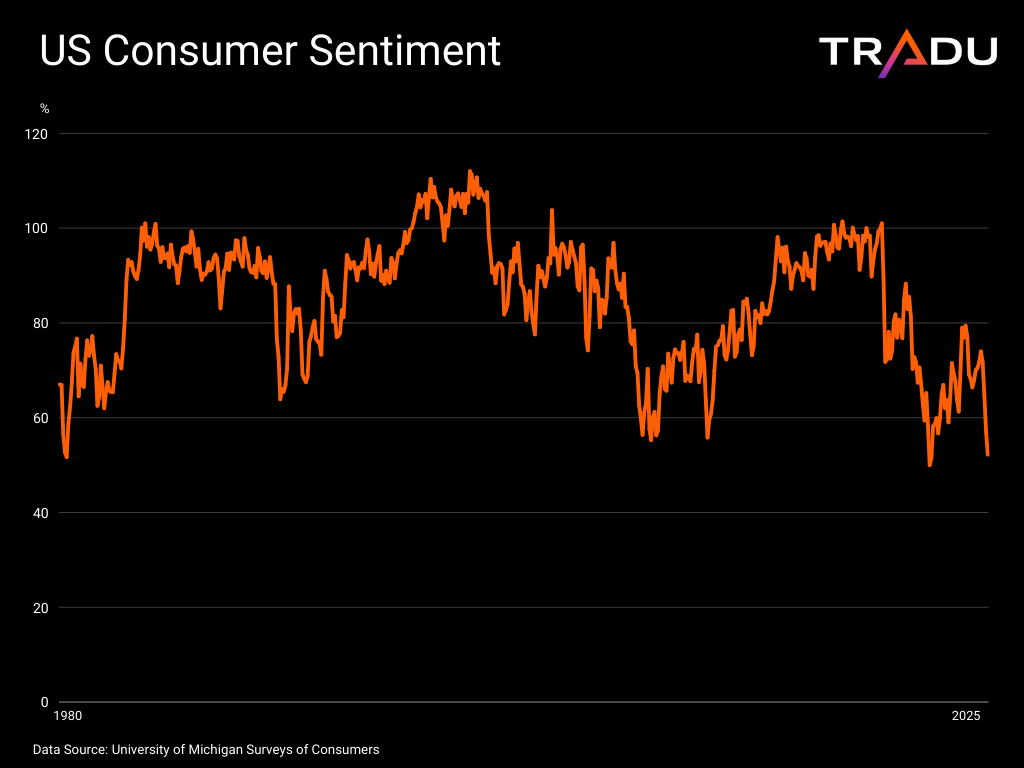

The decline adds to a series of deteriorating soft data, pointing to weak consumer and business sentiment. The April S&P PMI revealed that sentiment among service providers had fallen to its lowest level in two and a half years - among the weakest readings since the pandemic [3]. The University of Michigan survey reported consumer sentiment at its second lowest reading since 1980, with long-term inflation expectations reaching a peak not seen since 1991 [4]. These trends are compounded by elevated borrowing costs, leaving many households struggling to meet financial obligations. Credit card delinquencies (90+ days) have surged to their highest level in 14 years.

Domestic demand and travel stocks at risk as US consumers pull back

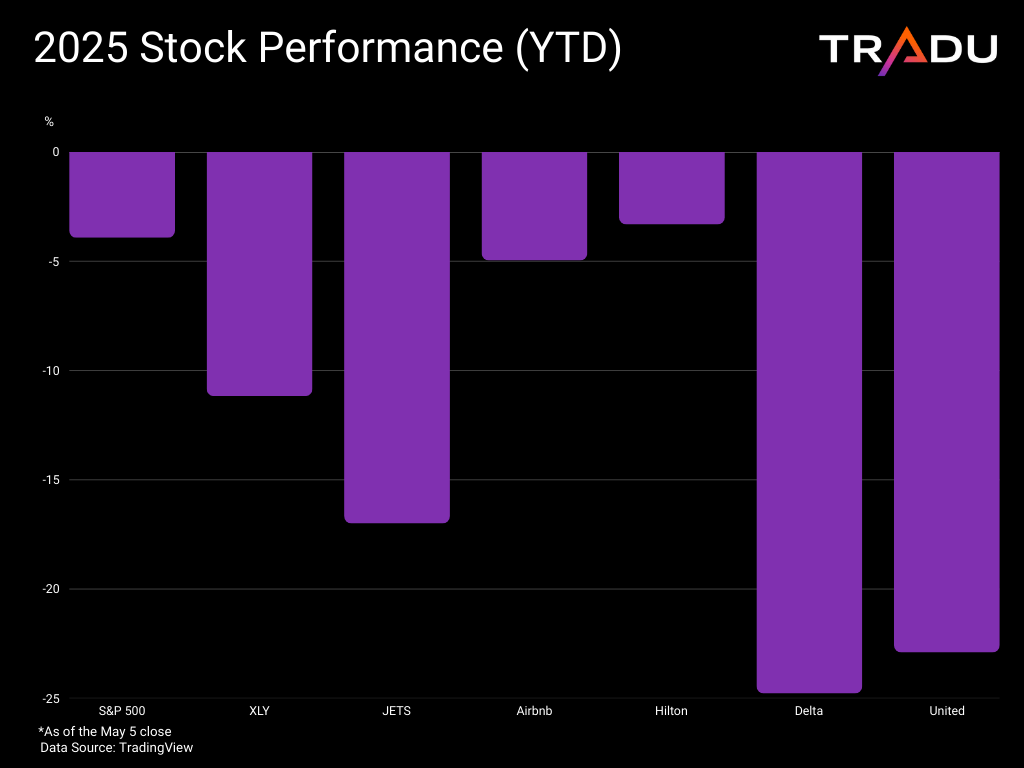

These actions have caused a steep decline in Wall Street this year, as they disrupt supply chains, can drive costs and price higher, while sapping demand. The consumer discretionary sector - which includes hospitality firms such as Hilton - has been the worst performer in the S&P 500, with the XLY ETF down 11.17% year-to-date. While airlines like Delta fall under the industrials sector, air travel is generally considered a non-essential expense, even if business travel can be less flexible with the JETS ETF falling 17%.

The US travel industry faces significant headwinds, as discretionary spending is typically the first to be curtailed by cash-strapped households in favour of essentials. Businesses also tend to reduce travel during economic downturns and periods of uncertainty. According to Bank of America, card spending on lodging and air travel has declined year-to-date through March compared to 2024 [6]. A survey by marketing and communications agency MMGY found that although 83% of US consumers still intend to travel within the next 12 months, 80% plan to adjust their behaviour—favouring shorter stays, more affordable transport, and other options.

Executives in the hospitality sector are seeing these changes first-hand. The Chief Financial Officer of online travel and lodging platform Booking.com noted during the latest earnings call a “decrease in length of stay in the US”, suggesting that consumers are becoming more cautious with their spending . Airbnb’s CFO also observed “relatively softer trends” in the US, driven largely by “broader economic uncertainty”, with consumers “waiting and seeing” before booking their summer travel [9]. Hilton CEO Chris Nassetta echoed these sentiments, noting a similar “wait-and-see mode” among travellers, particularly in the leisure segment. [10]

The US airline industry is also affected. Delta Air Lines CEO Ed Bastian was quite forthcoming, noting that growth has “largely stalled”, with the impact mostly felt in the domestic market [11]. His United Airlines counterpart Scott Kirby took note of “softer demand” due to “softer macroeconomic environment”, with his CFO pinpointing the “bulk” of the issue on domestic flights.

International tourism to the US declines amid trade tensions

In addition to domestic travel challenges, the US is becoming a less attractive destination for foreign tourists. This sentiment has been exacerbated by his territorial claims regarding Greenland and Canada [14], alongside stricter border policies. Germany and the UK, for example, have issued travel advisories or warnings, according to Reuters. [15],

Data indicate a clear shift: overseas visitors to the US fell by 11.6% year-on-year in March [17]. The number of Canadians returning from land trips to the United States slumped 31.9% in the same month [18], while Cirium points to reduced airline capacity between the two countries [19]. This is significant, as Canada remains the largest source of international visitors to the US. The US Travel Association has warned that a 10% decline could equate to $2.1 billion in lost spending and 14,000 job losses.

Airbnb CFO highlighted the diminished appeal, noting a “decline in popularity of foreign travelers coming to the US”. In similar vein, her Booking counterpart saw a “moderation in trends for inbound travel” into the country.

US travel companies face headwinds from deteriorating macros

The combination of tariffs, domestic consumer caution, and declining international demand is creating a challenging environment for US carriers and hospitality providers.

Airbnb revenues rose just 6% year-on-year in Q1 - its slowest growth in four years. Average daily rates (ADR) declined, and management expects them to be “approximately flat” in the second quarter. Still, the company maintained its 2025 outlook, projecting a sizable adjusted EBITDA margin of at least 34.5%. [21]

Hotel giant Hilton lowered its full-year guidance for revenue per available room (RevPAR) growth to 0%–2%, down from the 2.7% increase seen in 2024. Net income forecasts have also been reduced to between $1.707 billion and $1.749 billion. Despite this, both figures remain above last year’s results, showing a degree of resilience.

Delta Air Lines has withdrawn its 2025 guidance entirely. Its Q1 sales rose slightly—just over 2% year-on-year—while operating income fell by 7% [3]. United Airlines took the unusual step of issuing dual guidance, reflecting macroeconomic uncertainty. In a recessionary scenario, it expects adjusted earnings per share of $7–$9 in 2025 - at least 15% below 2024 levels . However, both airlines are reducing capacity to protect margins, showing that they have tools to whether the adversities.

US travel industry shows resilience despite challenges

The US tourism industry is under pressure from multiple fronts - falling domestic demand, reduced international arrivals, and economic instability. Airlines and hospitality firms are already adjusting by lowering or withdrawing their financial guidance. These difficulties are also reflected in their share prices: ABNB, HLT, DAL, and UAL are all down year-to-date.

Nevertheless, these headwinds may prove temporary. The tariff-induced uncertainty could be easing as the White House pursues new trade agreements. Additionally, US consumers - particularly those in higher-income brackets - continue to show resilience, which could support ongoing travel demand. This trend aligns with the premiumisation strategies employed by carriers like Delta and United. Moreover, global exposure may act as a buffer, with international travel appearing to hold up better.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.