Shares

Moment of truth for the Magnificent Seven: Meta, Microsoft, Apple, and Amazon to report earnings

Big Tech is reeling from Donald Trump’s disruptive trade policies, which have rattled Wall Street, while rapid advances by Chinese rivals are challenging US dominance in artificial intelligence (AI). Against this turbulent backdrop, four members of the Magnificent Seven - Meta, Microsoft, Apple, and Amazon - are set to report pivotal quarterly results that could define their stock trajectories.

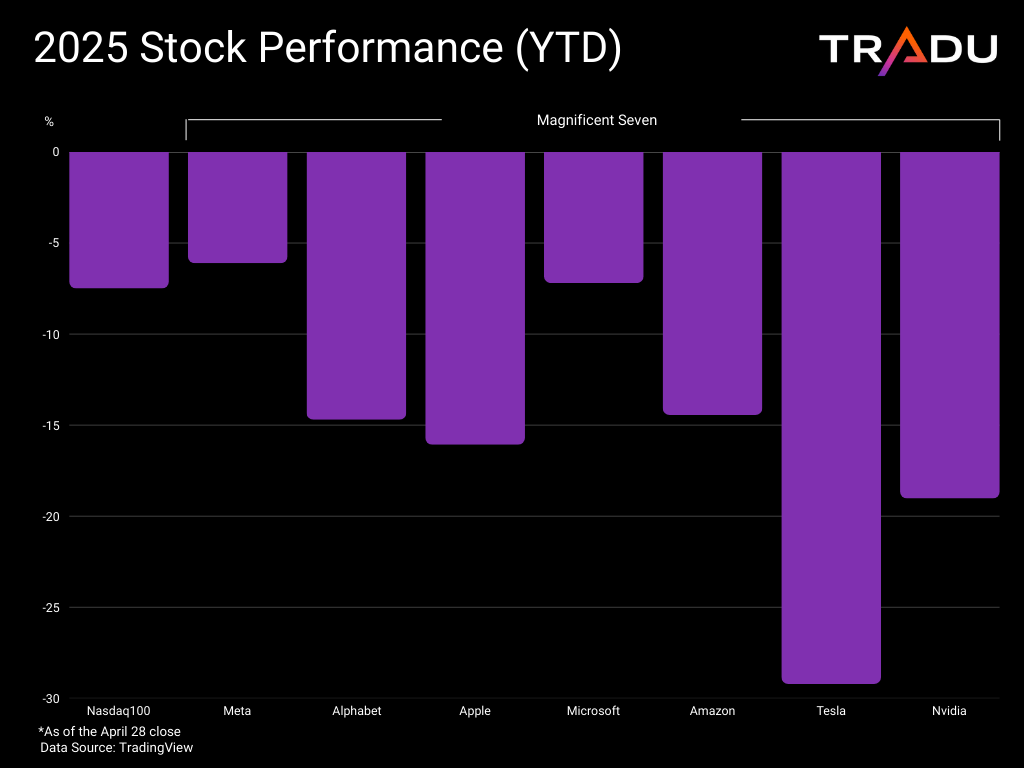

Magnificent Seven stocks on the back foot ahead of key earnings

Although some prominent tech names are performing well this year – such as streaming giant Netflix and enterprise AI leader Palantir – the broader Magnificent Seven are slumping. Shares of Meta Platforms, Alphabet, Apple, Microsoft, Amazon, Tesla, and Nvidia all record steep year-to-date declines.

DeepSeek’s breakthrough low-cost AI model and the subsequent rapid advancement of Chinese giants like Alibaba and Baidu are challenging the US Big Tech AI dominance, while questioning the need of their massive infrastructure investments. At the same time, Trump’s tariffs threaten economic slowdown, demand for their products, and their financials, while regulatory challenges at home and abroad remain.

Tesla kicked off the earnings season for the Magnificent Seven with disappointing results, though Elon Musk’s renewed focus on the company and new self-driving regulations from the Department of Transportation have helped the stock recover somewhat. Alphabet reported stronger figures [1], but signs of slowing growth in cloud and advertising revenue have raised caution.

Attention now shifts to Meta, Microsoft, Apple, and Amazon, all set to report this week. Markets will closely watch for any commentary on how deteriorating macroeconomic conditions are impacting advertising spend – a significant revenue stream. Updates on capital expenditure and the financial benefits of AI will also be key themes. Strong results and guidance could instil some optimism and help shares recover, but disappointing updates could reignite bearish sentiment.

Meta’s AI leadership doesn’t spare it from the Big Tech slump

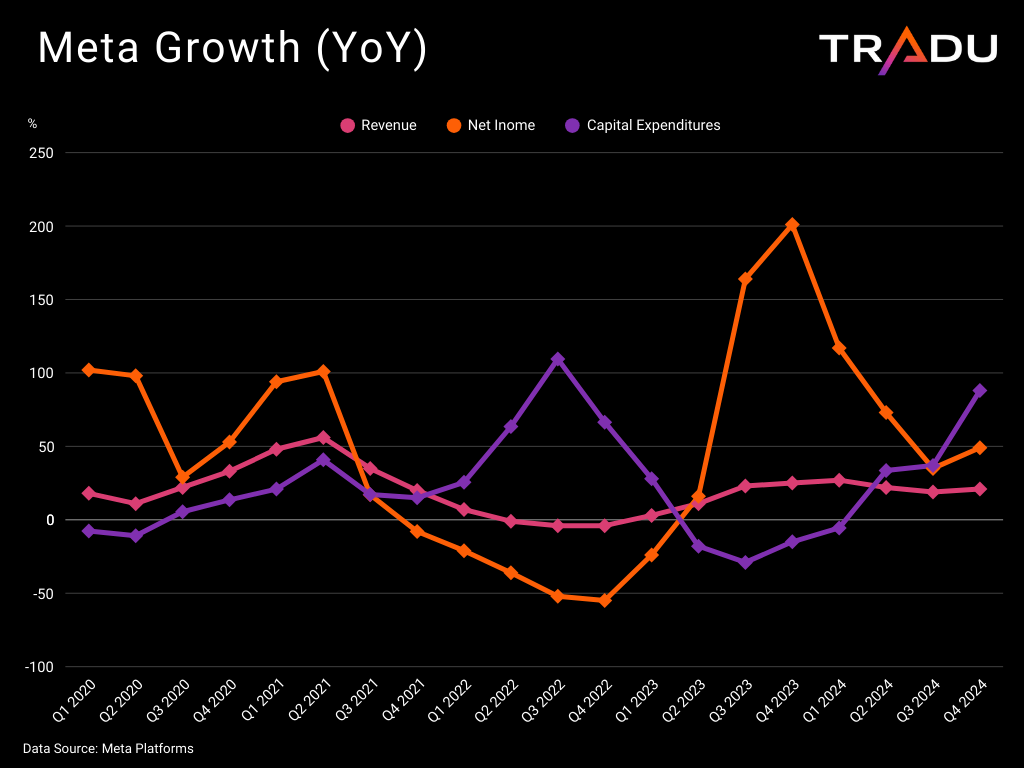

Meta Platforms has emerged as a leader in AI this year, thanks to Mark Zuckerberg’s strategic pivots, investments in the technology, and the decision to open-source its large language model (LLM). Management has highlighted increased user engagement and advertising demand from its AI tools [2]. Despite this, Meta has not escaped the Magnificent Seven’s slump, with its stock down around 6% year-to-date as risks loom

Revenue growth has stagnated, and management anticipates a slowdown to 8%-15% year-on-year in Q1 – the weakest pace in nearly two years [3]. Any further advertising weakness due to macroeconomic uncertainty could intensify headwinds. A reaffirmation or increase in its target of at least 50% year-on-year growth in annual spending may signal confidence in AI, but could also unsettle investors. In a challenging economic environment with slowing sales, the market may favour a renewed focus on efficiency over heavy AI investment. Additionally, Meta’s bet on open-source models has served it well so far but could inhibit its ability to monetise AI advancements effectively.

Microsoft vulnerable as AI edge diminishes

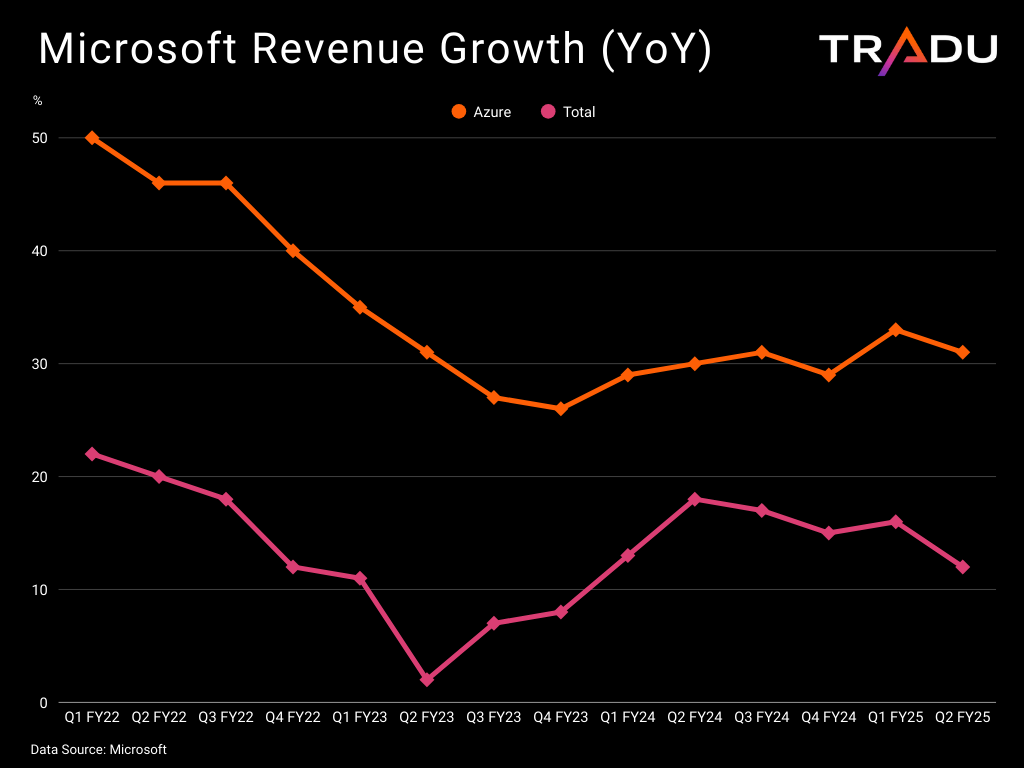

Microsoft was an early AI winner thanks to its investment in OpenAI, which triggered the current AI wave via ChatGPT. However, its lead is narrowing as rivals catch up, particularly in Agentic AI, where Salesforce is making significant strides. MSFT follows peers lower this year, with losses of around 7%.

The tech juggernaut has not been able to demonstrate convincing return on its AI investment, with its last results and guidance disappointing markets [4]. Sales of Azure underwhelmed, while overall revenue growth decelerated, and the company expects further slowdown in the reported quarter (Q3 FY2025). Although not as exposed to tariffs as other Magnificent Seven peers, the challenging external backdrop and its own inadequacies increase monetization pressure.

Apple faces existential threats from tariffs and AI lag

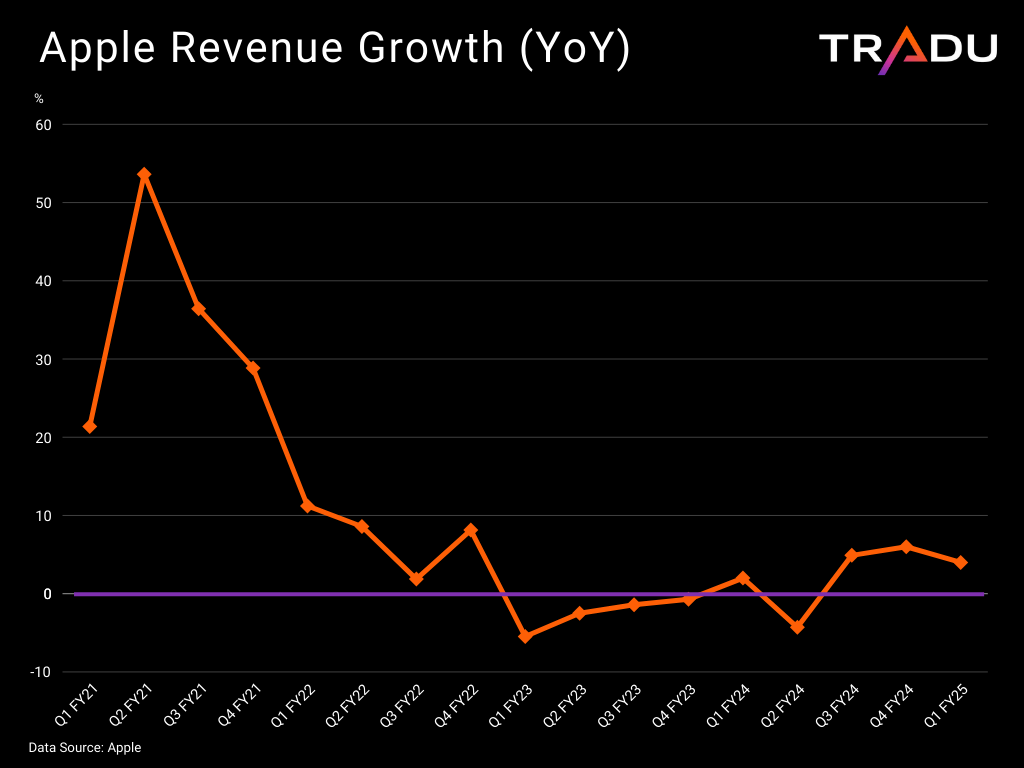

Apple is the most vulnerable Mag7 member to Trump’s tariffs and the trade dispute with China, due to its substantial manufacturing footprint and customer base in China. Although it got a temporary reprieve from the pause in smartphone levies, President Trump has hinted at more trade actions ahead. These concerns add to existing pressures from weak Chinese demand and an underwhelming AI rollout, fuelling perceptions of declining innovation.

The impact is evident in Apple’s share price – down over 15% year-to-date – and its sluggish revenue performance. Management expects this disappointing trend to continue in Q2 FY2025 [5], underlining the challenging backdrop. Poor guidance could deepen investor concerns. Still, Apple’s margins remain healthy, and potential price increases could pull forward consumer demand. Furthermore, the upcoming Worldwide Developers Conference (WWDC) offers an opportunity to showcase AI progress.

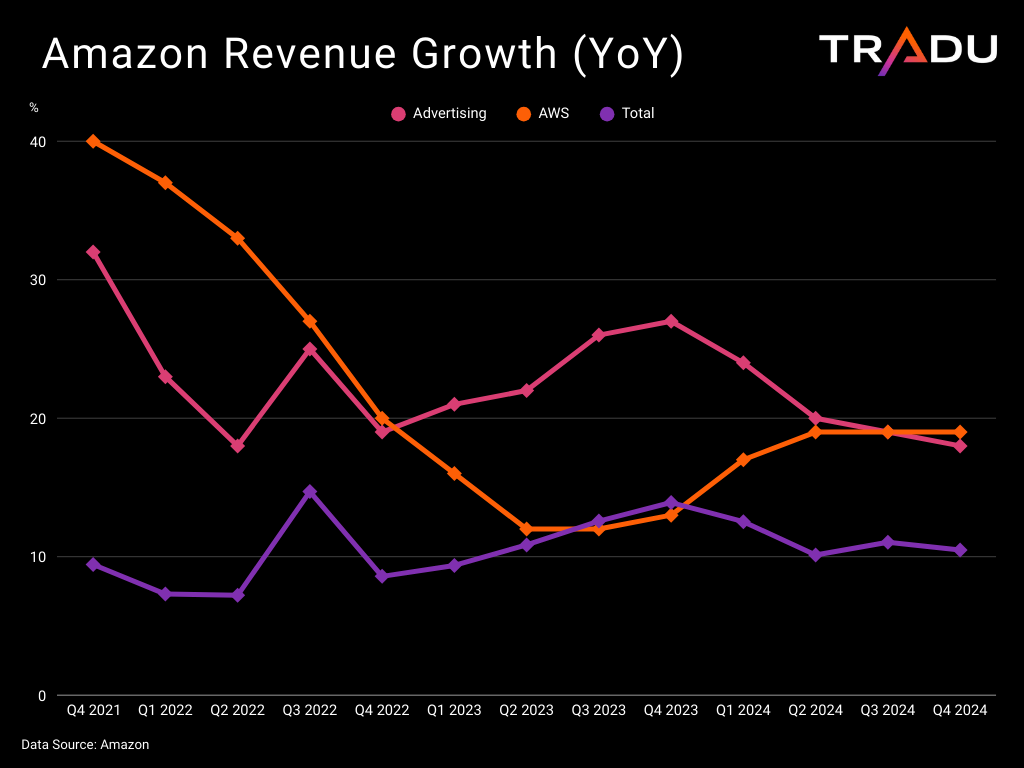

Amazon playing catch-up in Artificial Intelligence

Even though Amazon is launching its own generative models and leverages the technology to enhance its cloud and advertising sales, it does not appear to be at the forefront of innovation, which may place it at a disadvantage. This exacerbates concerns over stagnant cloud revenues, with overall revenue growth expected to slow to 5%-9% in Q1 2025. [6]

A global economic slowdown could dent its advertising revenues, while trade disruptions threaten its ecommerce business. Domestic risks such as stagflation and weak consumer sentiment may also weigh on sales. Any further signs of weakness could increase pressure on the stock, which is down roughly 15% year-to-date.

However, Amazon’s scale and diversified business model could help it weather the storm. It may even benefit from changes to de minimis import rules [7], which could impact Chinese competitors like Temu more heavily.

Magnificent Seven face near-term headwinds, but long-term strength remains

Meta Platforms, Microsoft, Apple, and Amazon approach their earnings reports from a position of relative weakness. Trade disruptions, economic uncertainty, and challenges to their AI leadership are all creating financial and stock market pressures.

Nonetheless, the Magnificent Seven are well-placed to weather these difficulties. Despite near-term headwinds, they remain structurally strong and could retain their dominant position in the long run. Additionally, more attractive valuations may start to renew investor interest in their shares.

Senior Financial Editorial Writer

Nikos Tzabouras

Nikos Tzabouras is a graduate of the Department of International & European Economic Studies at the Athens University of Economics and Business. With extensive experience in market analysis and a strong foundation in international relations, he brings a unique perspective to financial markets. Nikos emphasizes not only technical analysis but also on fundamentals and the growing influence of geopolitics on financial trends.

As a Senior Financial Editorial Writer, he delivers comprehensive and forward-looking insights across a wide range of asset classes, including equities, commodities, and currencies. His work explores how macroeconomic events, political developments, and global policies impact market dynamics, providing readers with a deeper understanding of both short-term movements and long-term trends.